Sabitlenmiş Tweet

Eli5DeFi

46.8K posts

@Eli5defi

Visual Information Layer of Technology | TG Channel ➠ https://t.co/NquSvtqawK | Substack ➠ https://t.co/pMyJJEK8u6 | All Posts NFA + DYOR

The next generation of traders won’t trade manually, they’ll deploy agents. Beep is partnering with @BitgetWallet to onboard the next wave of Agent Traders. $35,000 in rewards is now live: • $30,000 user reward pool • $5,000 trading leaderboard • 2x Beeper Points multiplier for Bitget Wallet users Users can now create their first AI trading agent on Beep for free through Bitget Wallet, deposit, and execute trades across AI Trading and Predict Agent. Deploy your first agent now: newshare.bwb.global/en/earnCoinsTa…

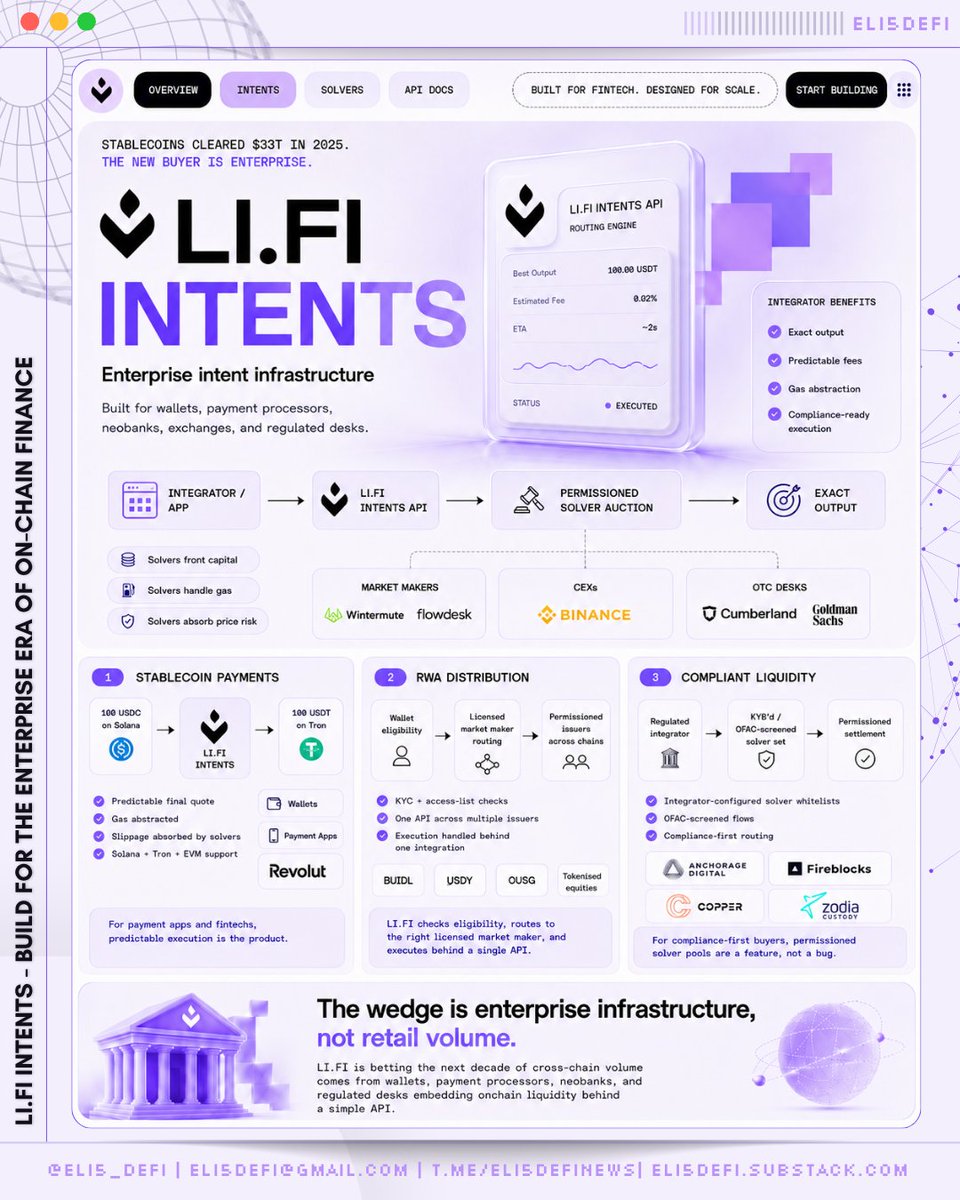

Introducing LI.FI Intents. Infrastructure for apps, wallets, and neobanks to: • Enable stablecoin payments • Access real-world assets • Tap into compliant onchain liquidity Built for enterprises bringing financial products onchain.

Kinda insane watching Ferrari go from: "you'll have to shoot me before we make an EV" to "okay guys but what if the electric car had REALLY satisfying buttons" 😭 Did some reading on the new @Ferrari EV launch today & this might be one of the biggest “brand identity stress test” and why🧵

Most AI agents today don't pay for themselves. They run on someone's AWS account, an OpenAI key tied to a card, or a SaaS subscription billed to a person. Autonomous agents need autonomous payments, that's why we're introducing the Agent Survival Pack with launch rewards today 🧵👇

I was looking into Solstice float (95%+ held by team & insiders) & came across a wallet that dumped $645K worth of $SLX on-chain, causing the SLX token to crash the wallet received 5M SLX from a team wallet two days ago: HAqfsvUjpRsGxPKb43j78dQ8WgKDutnxKaLjy6fp42ya the address bridged 3.5M SLX from Solana to BSC and has dumped 3.02M tokens so far (still holding the rest) BSC address: 0x6d04698d42950cc1eb6abc26a9ec32521f5a3e77 it also sent 1.5M SLX on Solana to Gate & Bitget deposit addresses. at first i thought it might be for liquidity, but they may have dumped there as well the same BSC address also received 700K OG (~$1.9M) bridged from OG Chain via LZ and deposited it to Binance 7 months ago after checking activity on OG Lab Chain, the wallet appears to have previously transferred OG tokens to multiple exchanges (likely for market making), so i suspect the wallet belongs to their MM @solsticefi