Sai Lavu

125 posts

Where do the 40+ ladies take their energy from? I have one at home - it is curse and blessing at the same time. Perimenopause is a threat for your family life and your relationship 😂

English

@SystematicPeter Great insights. I’ve taken your blueprint and working further with it. Thanks for sharing. I’ll share back when I get it to a stable state.

English

Intraday Volatility Breakout Blueprint

crackingmarkets.com/intraday-volat…

English

Most intraday breakout strategies fail for one boring reason: costs were guessed, not measured.

If you trade intraday volatility breakouts (like in my Intraday Volatility Breakout Blueprint), you must model slippage and commissions precisely. Otherwise, your edge is fictional.

I pulled the stats from my live execution on SPY and QQQ.

Reality check:

- Average realized slippage is ~1.5 ticks round turn

This is not theoretical. This is the benchmark your backtest must survive.

Important note for smaller accounts:

Intraday systems rely on small stops and higher notional exposure. With ETFs, that quickly becomes capital-intensive.

If capital is a constraint, do not get stuck.

The exact same logic works with futures.

MES (Micro S&P) and MNQ (Micro Nasdaq) offer:

- Low margin requirements

- Efficient position sizing

- Identical strategy logic

Account size should never be the reason you avoid being systematic.

English

@UnForgeron True. But it’s not that exciting for us when the systems are running. You lose track of tickers in play.

English

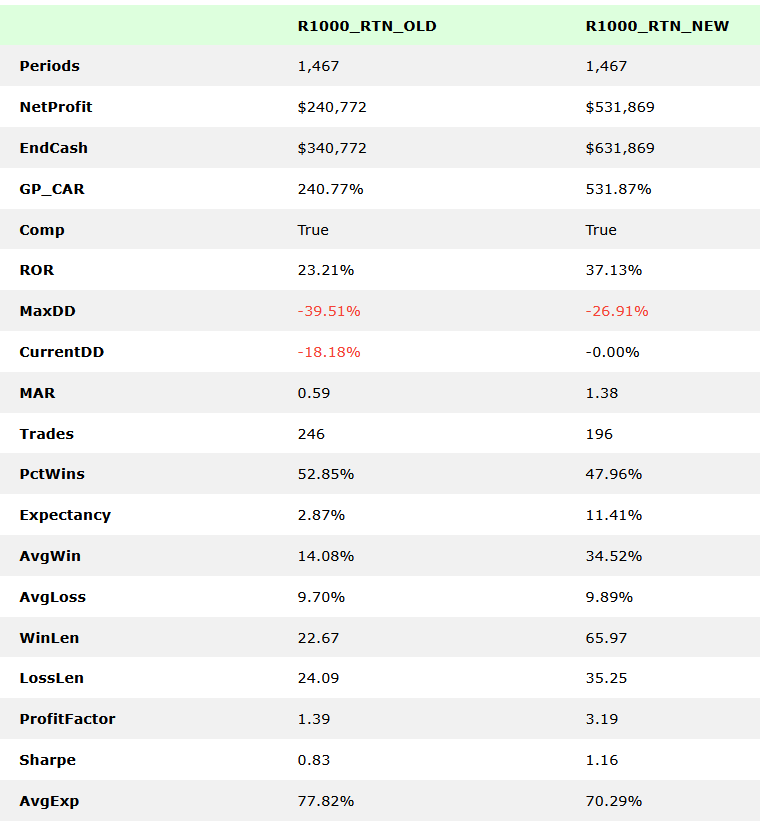

@sailavu Exposure for the OLD system was 77%

Exposure for the NEW system is 70%

So the new system has less exposure to the market, due to the addition of the $SPX Volatility Regime Filter, which will take the system to a position of CASH, during periods of increased VOLA in the market.👍

English

OCTOBER 2025 Stats

WTT -9.98%

ASX LSS +0.22%

US LSS +3.55%

MR#1 +4.66%

MR#2 +7.13%

MR#3 +4.52%

Monthly Rotational Systems

ASX100 RTN -8.11%

XSO RTN -11.99%

NDX100 RTN +7.53%

R1000 RTN +18.60%

ASX ALL Weather +4.0%

#Next1000Trades

English

@LeTourTrader Good effort. What was the volatility of the strat before and after the change? I wonder how the increase in holding period changed it. Longer holds may mean handling more volatility.

English

Zoomed in comparison of the last 6 years

1/1/2020 - 31/10/2025

Note the increase in hold time between the OLD & NEW systems

Hold time 22 (OLD) -> 65 (NEW)

Average Win goes from 14% (OLD) - > 34% (NEW)

Profit Factor 1.39 (OLD) -> 3.19 (NEW)

English

@PKycek @MetroTul @robuxio_com Can attest that the above statement is correct and also the DD. Thought the portfolio would be wiped but when I checked this morning it has held up.

English

@MetroTul @robuxio_com Nope, we made some money. But we accumulated significant DD before.

English

Momentum short strategies have a weak edge on crypto.

Most of the time they act as in insurance policy - you slowly lose money - paying for the protection.

From time to time, your insurance is paid.

English

@danw_trades That’s amazing. Once you set up the automation it works great. Not quite as many Strats and currencies but likely get there soon’ish with futures

English

@UnForgeron Same boat as you. Will share what I learn. Thanks @danw_trades for the tips.

English

WTF! Is Nasdaq a serious exchange? $CURX "The company was founded by Ying Jing and Chang Liu ..."

English

@sailavu Options: Trading Strategy and Risk Management, By Simon Vine

and

Sheldon Natenberg Option Volatility and Pricing: Advanced Trading Strategies and Techniques, 2nd Edition

Have been two recommendations that I have received

English

Systematic Options Traders - what are your recommended resources for someone that knows 0 about options?

Currently I have ordinary stock, etf and crypto portfolios and I was interested in exploring options as another way of diversifying systems.

English

@UnForgeron RealTest GPT is handy to use within ChatGPT (search within the forum). I use a combination of Claude and ChatGPT (have paid edition).

English

@PrimeTrading_ @alphacharts365 @GregDuncan_ Dexcom is pretty good (used by lot of Type 1 as it links to the insulin pumps) and so is freestyle libre. It has been a game changer to understand what causes spikes and what doesn’t. Looping in dietician support (1-2 visits) is valuable too. Good luck.

English

@alphacharts365 @GregDuncan_ We need to go long $DXCM boys

English

Hey @GregDuncan_ I’m starting tonight! Thanks for the idea, I’ve been meaning to see hard data about how the foods I eat affects my blood sugar and now I’ll know.

English

@SystematicPeter I used to do this on a discretionary basis. My edge was: 1. acting right after the earnings during pre or after mkt hrs, the initial burst in either direction, 2. trade during the market hours after a pullback from the open. Is on my list to explore systematically.

English

Most traders ignore post-earnings moves… but they seem to be a goldmine when traded systematically.

Just saw this verified Kinfo trader:

kinfo.com/portfolio/3006…

— likely trading long/short equities right after earnings, holding for just one day.

No CAGR or Sharpe shown, but the equity curve speaks for itself.

Anyone in my network running a post-earnings systematic strategy?

English

@JoachimMo1985 Good to know. This is Market order I presume not MOO order?

English

You might not get the open price when trading odd lot orders even in high liquid stocks also in SPX/NDX stocks.

English

@stochastic_dev Nice work. Are there other systems that complement this system given the no of DD days? Gets tricky otherwise to keep pushing buttons when you are in the midst of it. It is a stat I am focusing on improving too across my Strats.

English

If your broker calls you to invite you to a conference, you know you are paying too much comissions. 🤪

English

Thank god $AXON is gapping up today after big earnings beat. Momentum position and MR strategy opened a position too.

English

@UnForgeron Worth checking out smartsystematictrading.com/product/smart-… and chat to @HelixTrader (the author of the tool). Should work out given your stack.

I am on a different stack (RealTest, Norgate & Alpaca) and need custom Python code to automate it. Doing it manually sucks imho.

English

@SwarmQuant @JoachimMo1985 May I ask what do you use for testing intraday strats? I find TV not the right tool for it as well.

English

@JoachimMo1985 TradingView is really not the right platform for this.

It is good to get a quick visualization to see if your functions work like intended.

English

To all systematic traders, how do you do robustness testing in TradingView? I was looking at some intraday strategy and imho it is a nightmare.

English