@Ren_aramb Thanks for the info then. I'm currently holding a small position so will probably buy the dip aswell

English

Seba Sonoqvist

132 posts

@sonoqvist

My thoughts. No investment advice. Investing in the techspace. Photonics, Memory and everything AI related

So just checked out the comments... $P4O does look like a potential upstream $LITE supplier at a $34M MC. How it likely maps: -> Plan Optik $P4O (Glass Wafers) -> Teledyne $TDY or Silek (Mem Foundries) -> $LITE (OCS Switches) -> $GOOGL (TPUs) However, $LITE likely dual sources with Corning ( $GLW ) on the glass wafer level. P4O is a known supplier to Infineon, Samsung, and others, so not exactly a random company. €3.35 million vs. 35.52M MC is very healthy balance sheet. That being said: -> That doesn't exactly mean this translates to material revenue boosts unless they start price hike (given glass wafers are likely a very small part of $LITE OCS BOM). I do personally own shares, after reading this. Since $LITE OCS potential supply chain chokepoints is strategically valuable. Maybe not so much so as financially valuable. But their core thesis that Plan Optik's Glass Flow and MDF finishing are effectively irreplaceable for OCS packaging checks out. Of course, hyperscaler supply chains are heavily guarded, so no way to know 100%. All credit goes to follower comments. But TLDR: Supply Chain Mapping -> $P4O -> Foundries -> $LITE -> $GOOGL is very likely from their analysis. As for being a chokepoint in $LITE OCS supply chain... dunno if it translates materially. Again, not recommending this at all. Just thought the $LITE OCS supply chain mapping like this very interesting, and that it would be a waste of the follower kinda posted all this work into the void.

Most investors see $M7U Nynomic as a struggling German industrial micro-cap. They're missing a near-monopoly quietly embedded inside it — one that sits at the heart of the AI datacenter buildout. Here's the full investment thesis 🧵

I recommend that everyone, especially with stocks where there’s a lot of writing and very little math, run a few scenarios for the future. Let’s take LPKF. Mega bull scenario for glass revenue (plateau from 2029–2030): LIDE equipment: 8 to 12 major customers scale into mass production, each needing 5 to 15 systems. At 20 to 40 new systems annually and €1.5 to 2.5M ASP, that’s €40 to 80M. Platform upsell (NeXaR Ablate, Bond, Direct Write): 2 to 3 additional systems per customer, adding €15 to 30M. Foundry services for smaller customers (quantum computing, MEMS, prototyping): €10 to 20M, limited by site capacity. Recurring revenue from an installed base of 80 to 150 systems (service, spare parts, upgrades): industry standard is 5 to 10% of installed value annually, so €10 to 25M. CPO/waveguide equipment, if adopted from 2028 to 2029: 5 to 10 Direct Write systems at €2 to 3M ASP, so €10 to 30M. Mega bull total: €85 to 185M annually from glass by 2030, a doubling of today’s total revenue, from the glass business alone, on top of the legacy business. What that means for valuation: At €150M glass revenue, 20% EBIT margin and 25x EBIT multiple, both optimistic, the glass business alone would be worth ~€750M. With the market cap already at ~€470M today, I don’t see 10x potential here. Even in this wildly optimistic mega bull scenario, we’re looking at a 1.5x at most. And that assumes every single optimistic assumption plays out simultaneously. Does anyone have an even more optimistic revenue forecast they’d like to share and walk me through? I’d be happy to take a look and potentially revise my assessment.

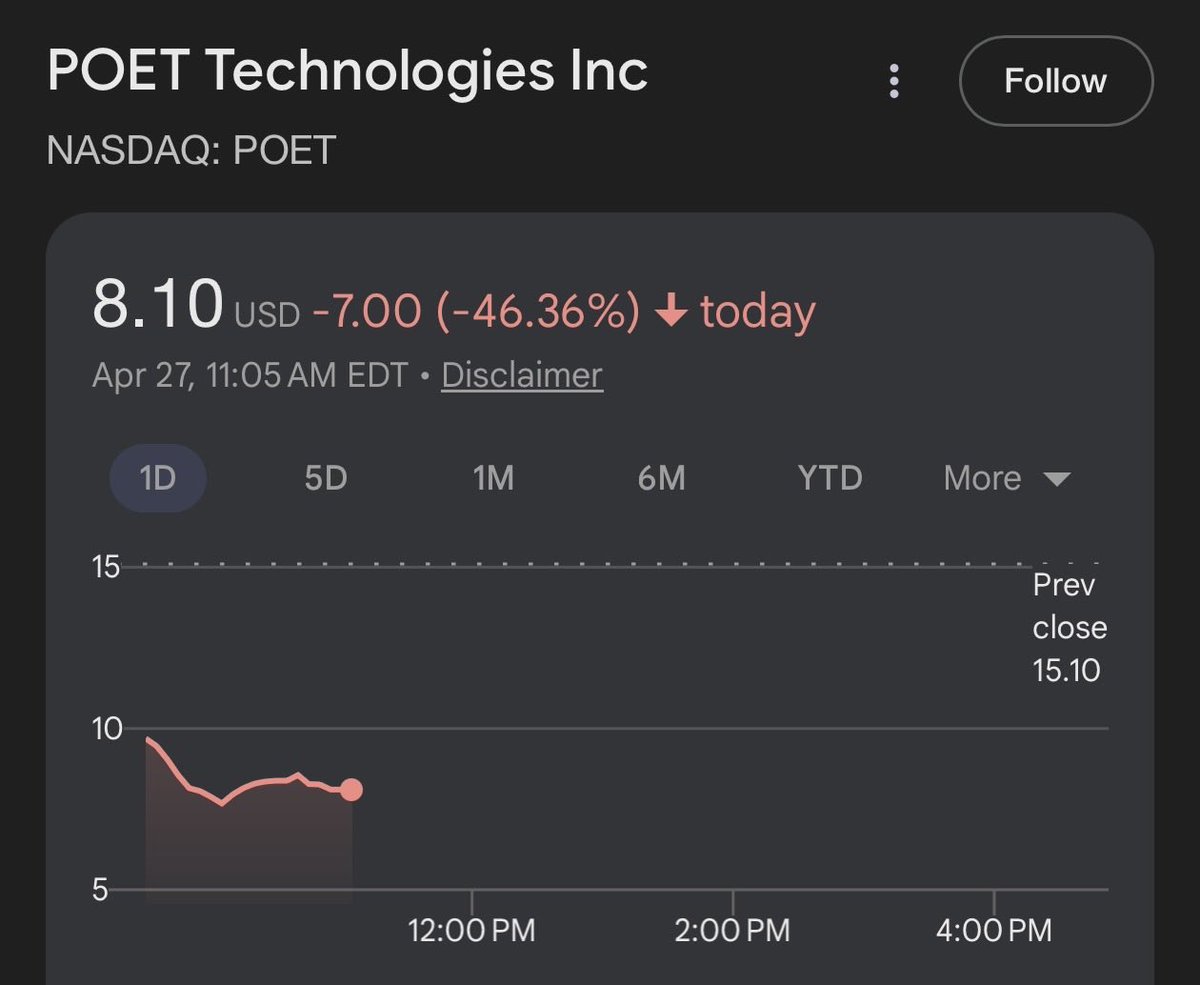

$LPK It seems the upcoming earnings are such a gamble. I see many potential vectors for positive developments, but on another note, such developments have become increasingly hard to qualify for the masses because of all the hype and false perceptions around the stock. The expectations are high. I mean we genuinely have people confusing T-glass and glass substrates, people thinking LPKF is the next $MRVL or $POET, etc. It's gotten to a point where we have "centralized investing", i.e., everyone will rely on a furu or a big account to interpret the earnings for them, and the reaction will proceed from there. A potential rally can happen only if a furu gives the green light because nobody knows how to interpret the earnings results for themselves

LPKF Laser are kinda interesting. Initial notes are: -> Owns LIDE - only 2-step laser + etch process hitting 5µm vias at 50:1 AR on glass panels. -> Every serious glass substrate player (SEMCO, SKC Absolics, LG Innotek, DNP, Intel) is a customer, partner, or in qualification. -> Their LIDE process is the only one hitting the spec envelope $AVGO/ $AAPL/ $NVDA ASICs actually require? -> €337M MC - seems to be priced as a solar-drag industrial laser co. Not as a chokepoint of the packaging transition. -> Pretty ugly P&L. I started a small position yesterday which I'll build out next week depending on how I feel when the time comes.

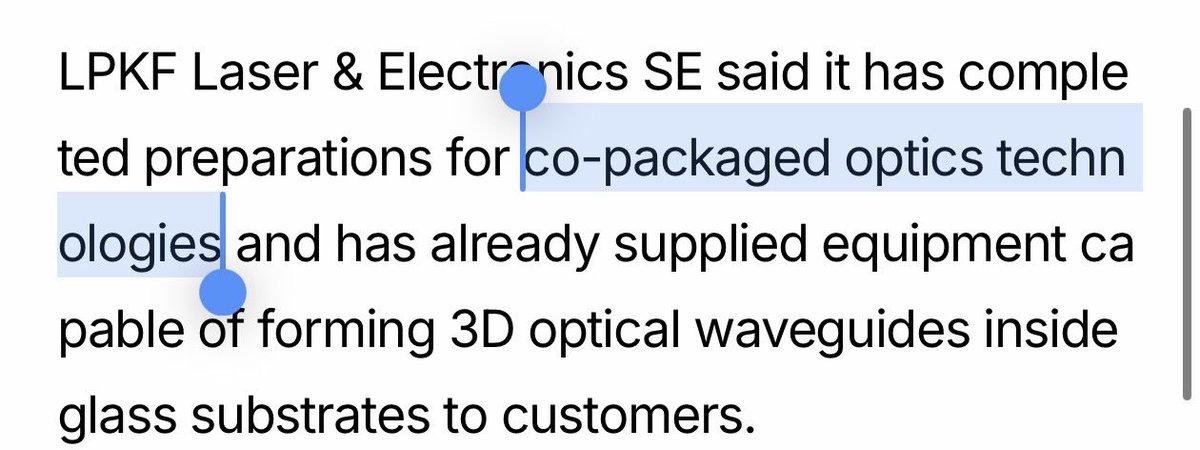

I do really like $LPK. Critical monopoly chokepoint in glass substrates… Which are used for advanced packaging and CPO. I flagged it as a potential 10x back in Jan, but thought it was a bit early. However… time seems right now? "About four years ago, we began collaborating with a semiconductor company to develop mass-production equipment for direct 3D waveguide formation," Lee said. “The customer has already installed LPKF's equipment." Maybe Samsung or SKC Absolics since this was in Korea? Seems like momentum is ramping up now though like $AEHR pre-earnings, not quite high volume (2027), but around this time felt compelling for me. During the transition from qualification/pilot -> high volume.

@aleabitoreddit $LPKF / $LPK positively surprised me today. It literally finished flat despite the correction across the rest of the market. There is buying pressure, and every dip is being bought

@aleabitoreddit Many of your names have pulled back into a nice buying zone.

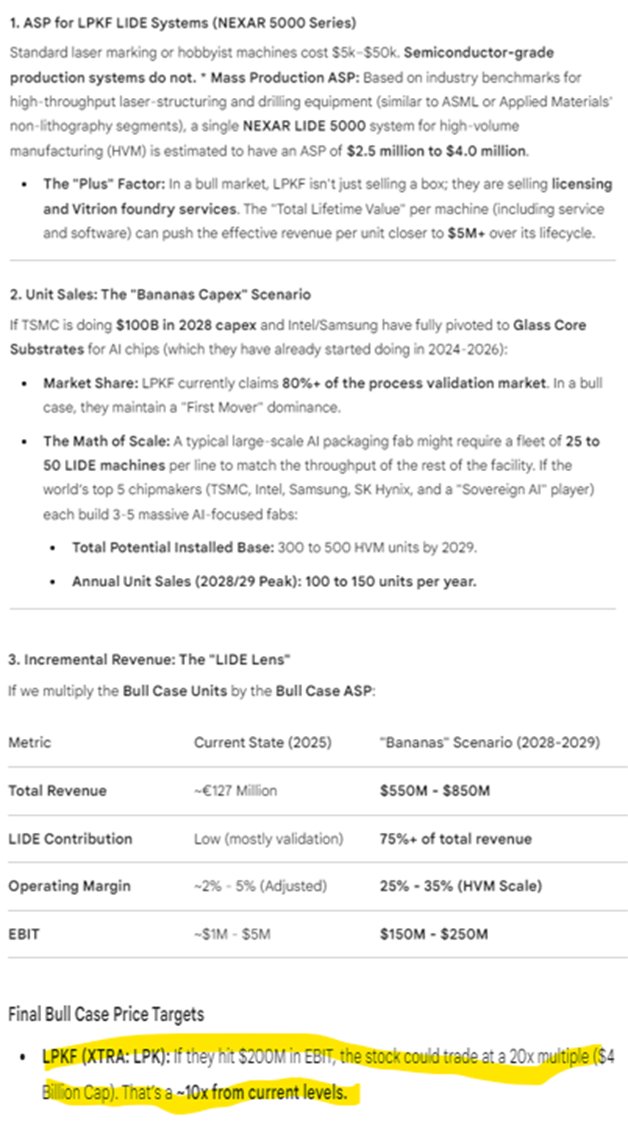

$lpk $lpkff 10x case with unit economics provided by Gemini AI Currently trading at <.5x 2028 sales and 1.5x 2028 EBIT in a strong AI Capex scenario... Much higher IMHO - I am long - NFA @aleabitoreddit @TheValueist