Will Ahmed@willahmed

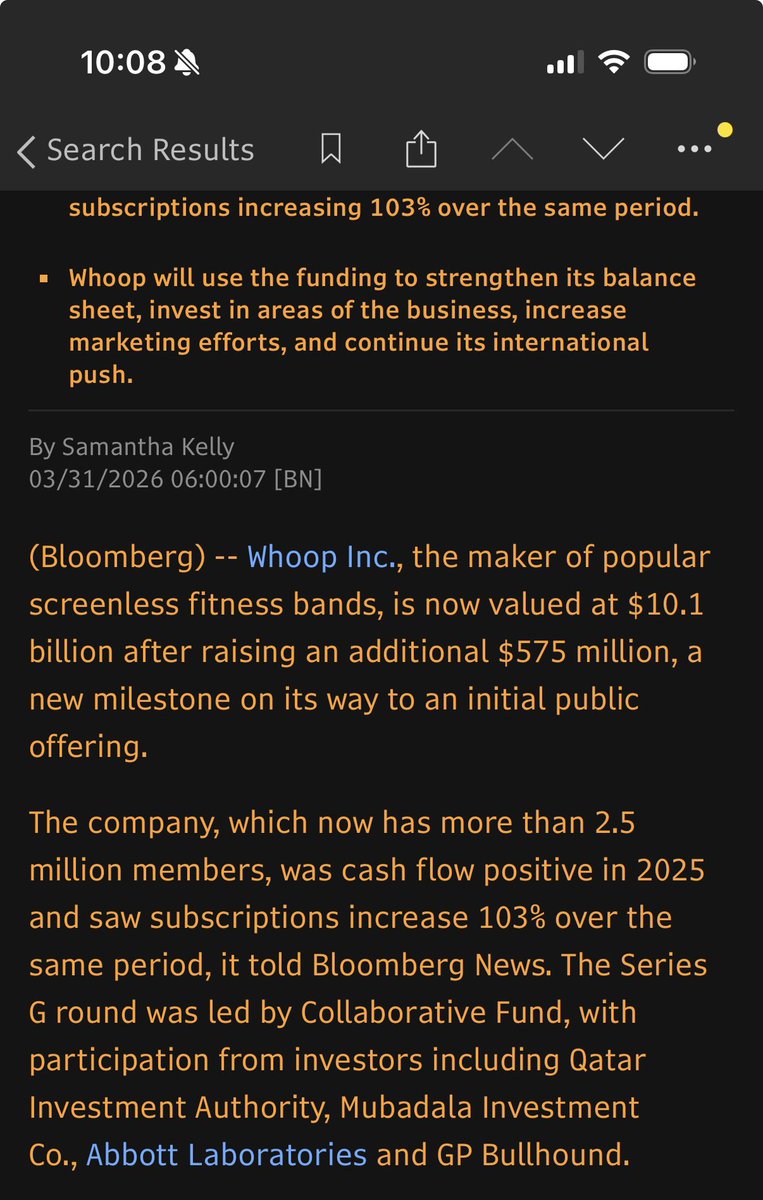

BREAKING: WHOOP RAISES $575M AT $10.1B VALUATION

I am pleased to announce that we’ve raised $575M at a $10.1B valuation to accelerate our mission of unlocking human performance and healthspan globally.

This round was led by Collaborative Fund with participation from 2PointZero Group, Qatar Investment Authority (QIA), Mubadala Investment Company, Abbott, Mayo Clinic, Macquarie Capital, Glade Brook, B-Flexion, IVP, Foundry, Accomplice, Affinity Partners, Promus Ventures, and Bullhound Capital alongside a group of individual investors including Cristiano Ronaldo, LeBron James, Rory McIlroy, Virgil van Dijk, and Mathieu van der Poel.

This investor group and this moment reflect a powerful evolution underway for Whoop and the broader healthcare market.

Whoop was born in performance - trusted by the best athletes in the world to train, recover, and compete at the highest level. That foundation remains core to who we are. You see that in the iconic athlete investors joining this round.

But it also represents our push into broader health.

In the past 12 months, WHOOP has received medical clearances, launched blood testing, and created a platform that has saved lives. Abbott and Mayo Clinic - two of the most respected and influential institutions in global healthcare - are now investors in Whoop. These are organizations that have shaped modern medicine. Their decision to partner with us is a clear validation of where our technology is headed.

Healthcare systems around the world are reactive. For too long, they have waited for people to get sick, then intervene. Chronic disease is rising and costs continue to climb.

At Whoop, we believe the future looks fundamentally different. We are building the most powerful, personal, preventive health platform in the world - powered by continuous biometric data, advanced analytics, and AI to help people understand their bodies and improve their health in real time.

I am grateful to our team, our members, and our partners for believing in this vision. I’ve been building this company for 14 years and I’ve never been more excited for the future.