@wealthmatica It's shaking out weak hands before we rip to the moon!

English

Delta Io

124 posts

$ZETA raised their 2028 revenue baseline to a 23% CAGR. Previously 20%. That’s a 3% uplift attributable to the Marigold acquisition. 2028 targets then present… - Core CAGR: 20% - Acquisition uplift: 3% It’s critical to keep in mind, this assumes… - Flat Marigold growth. - No beat/raise core revenues. - No political candidacy revenues. I assume with $ZETA's track record, they achieve closer to a combined 28-30% CAGR through 2028. - Core CAGR: 24-26% - Acquisition uplift: 4-6% And you’re bearish? $ZETA

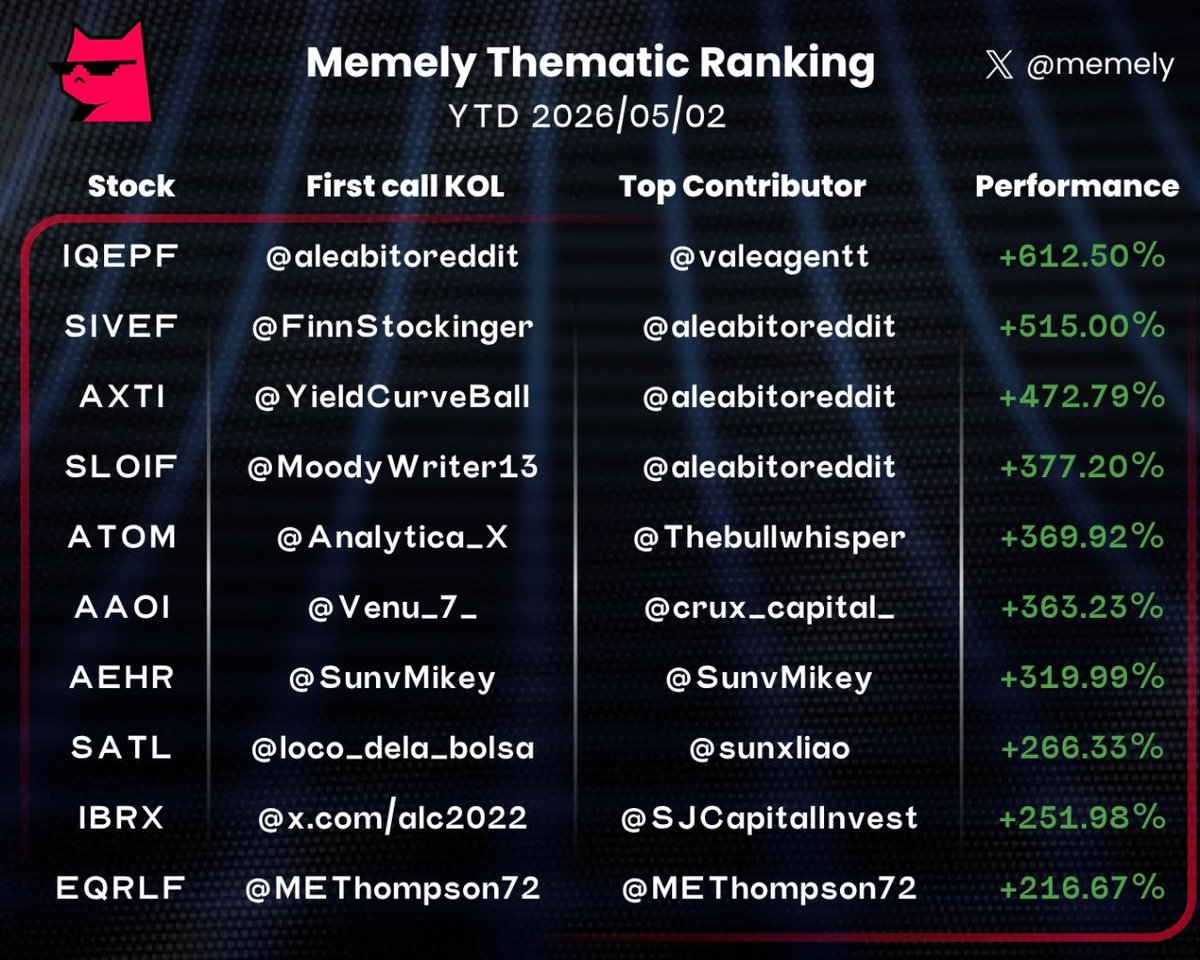

I guess, post earnings when $ARM touched $268... $ARM is now #18 on the individual stock list that I went long on that hit 100%-1000%+ YTD? I've lost count TBH. Some others like $LPK and $SIMO and $HPS.A are getting really close now. But feels like I'm one of the few ones out there on X with actual receipts of all the returns + original thesis post.

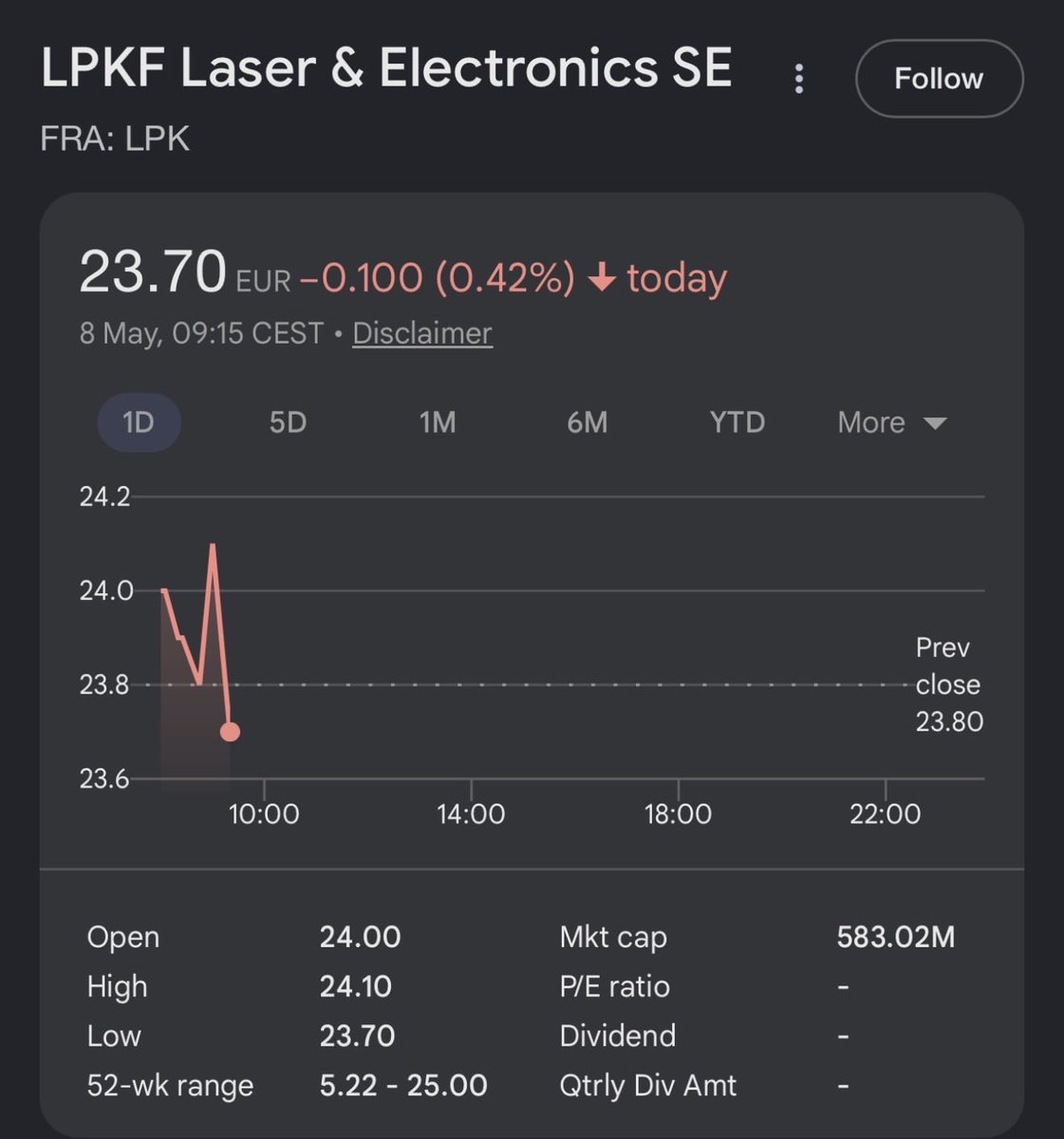

$LPK just confirmed they’re in talks for initial production system orders in advanced packaging. The rumor out of Germany is that one of those customers is a tier 1 US company. Intel is the most triangulated name. A 2023 patent explicitly describes LIDE-formed through-glass vias for a CPO architecture. Korean trade press named LPKF and SCHOTT as Intel’s glass substrate collaborators. And Fiedler himself referenced “more than two years of exclusive paid CPO development with a well-known larger US semiconductor partner.” Microsoft keeps coming up as well. They’re building their own silicon, they’re one of the most aggressive CPO adopters, and they have every incentive to lock in the equipment layer before the ramp gets crowded. Glass is emerging as the substrate best suited to keep 1.6T optics stable at scale. LPKF owns the drill.