RomainLedoux retweetledi

RomainLedoux

822 posts

RomainLedoux

@Romain_Ledoux_

Working on exiting Fiat. Bitcoin is the only open-monetary network upon which we can build back better

Montréal, Québec Katılım Eylül 2012

1.8K Takip Edilen386 Takipçiler

RomainLedoux retweetledi

Update. I don’t think it’s a structural moat though. If you look at Addendum 1, you can see that Microsoft expanded the contract by two tranches, but explicitly waived the upfront payment for those incremental tranches. To me, that tells me the 40% upfront on the original nine tranches was a Nebius-side requirement, and they negotiated that well. I would throw in that Microsoft was really capacity desperate in late 2025.

But as the addendum stated, if you look at January 2026, Microsoft was willing to pay for more capacity, but said no more upfront subsidy. And this is likely because Nebius now has Microsoft as a client and can raise debt or equity on different terms, not requiring prepayment.

So I don’t think this is a premium payment because of trust in Nebius, but more Microsoft financing their build at a moment of peak capacity scarcity. That’s what I see in Addendum 1 with zero upfront terms confirmed. Because the window confirming the addendum was closed within four months also.

$NBIS $MSFT $IREN $CRWV

@MB_Hogan

@daniel_koss

Markos@MarkosAAIG

“Microsoft GPU Servers at its new data center in Vineland, New Jersey over a five-year term. The Servers are being deployed in nine tranches during 2025 and 2026. Subject to the satisfaction of deployment and availability of the Microsoft GPU Services, Microsoft has committed to pay the Group fees under the Microsoft Agreement estimated to be up to $17,329.9, irrespective of actual utilization of the GPU capacity, including aggregate upfront payments of approximately $6,958.1, with the remaining consideration invoiced monthly over the service terms of the respective tranches through October 2031.” Very interesting that $NBIS landed higher pre-payments then the industry “standard” known to date. Is this a trend we will continue to see trough the industry? $IREN $CRWV

English

RomainLedoux retweetledi

$nbis Overlooked amidst recent press releases, co. dropped their 20-F late last week. Some news, confirmatory nuggets, & potential read-through for upcoming earnings:

1. Microsoft Deal:

--Upfront prepayment pegged @ ~40% of TCV ($6.95B on $17.39B contact value), which MStanley sees as significantly “higher than expected” and well above crwv’s referenced 15-25% prepayments

--Successful delivery of 2nd tranche from Vineland detailed against a 9 tranche delivery schedule; corroboration MS has contracted service-level credit compensation & termination rights

2. DC Strategy & Dev List

--Commentary on secured contracts across Europe, Middle East & US

3. Potential Benefits from Higher Pricing

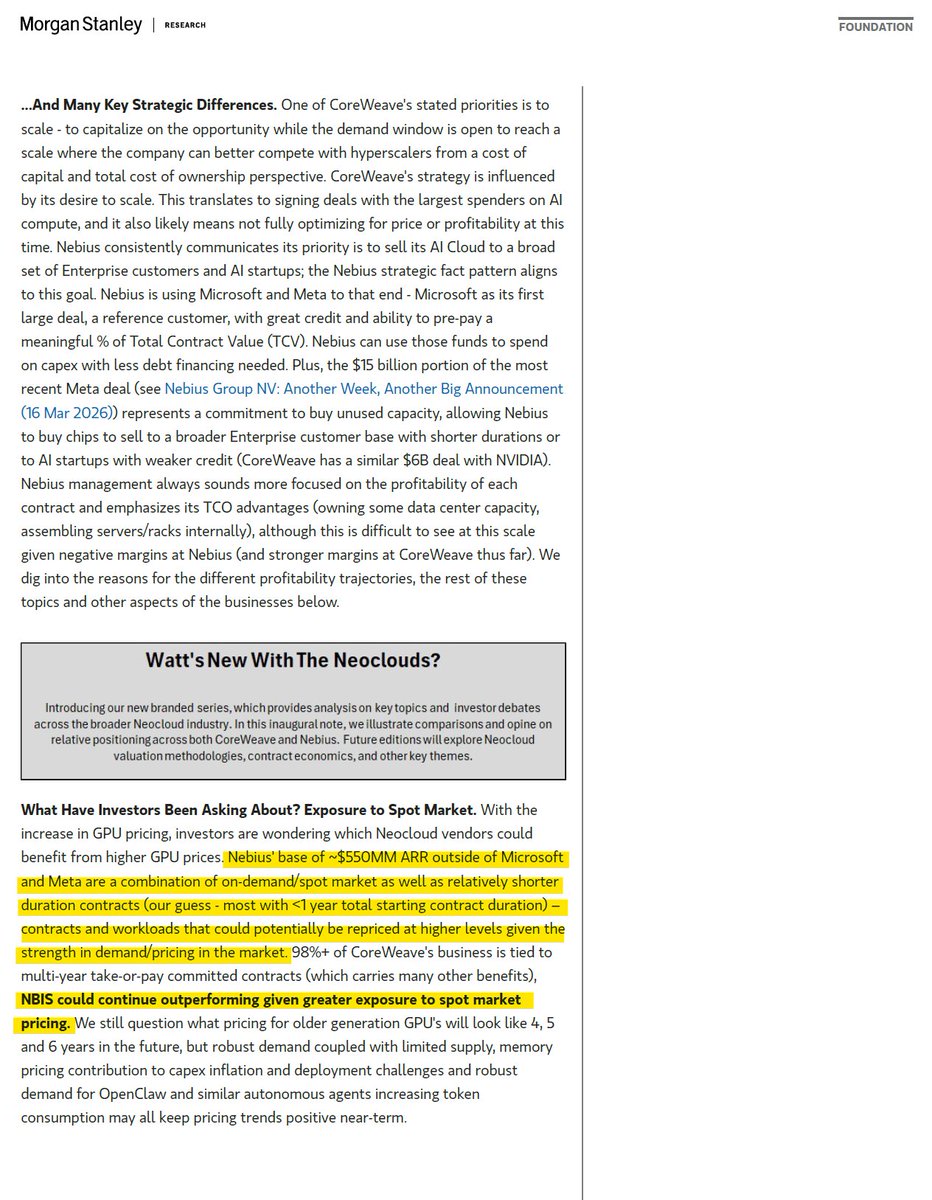

--Disclosure of a RPO @ $21.3B (pre-2nd Meta deal), plus a declaration that (outside Meta/Microsoft) “most of our customer engagements to date have relatively short term” implies possible read-through benefit from positive pricing trends

--In a note earlier this month, Mstanley marked Nebius's exposure to spot market pricing at its ~550M arr base, suggesting it could lead to near term “outperformance"

English

RomainLedoux retweetledi

Sweetwater 1 has been successfully energized – a key milestone in the development of the broader 2GW Sweetwater campus.

@danroberts0101, Co-Founder and Co-CEO of $IREN commented:

“Delivering Sweetwater 1 substation energization on schedule reflects our disciplined execution, the strength of our supply chain relationships and the efficiency of our vertically integrated development model. It is another example of our ability to design and construct large-scale infrastructure reliably and at speed to meet market demand.”

Learn more: iren.gcs-web.com/static-files/d…

English

RomainLedoux retweetledi

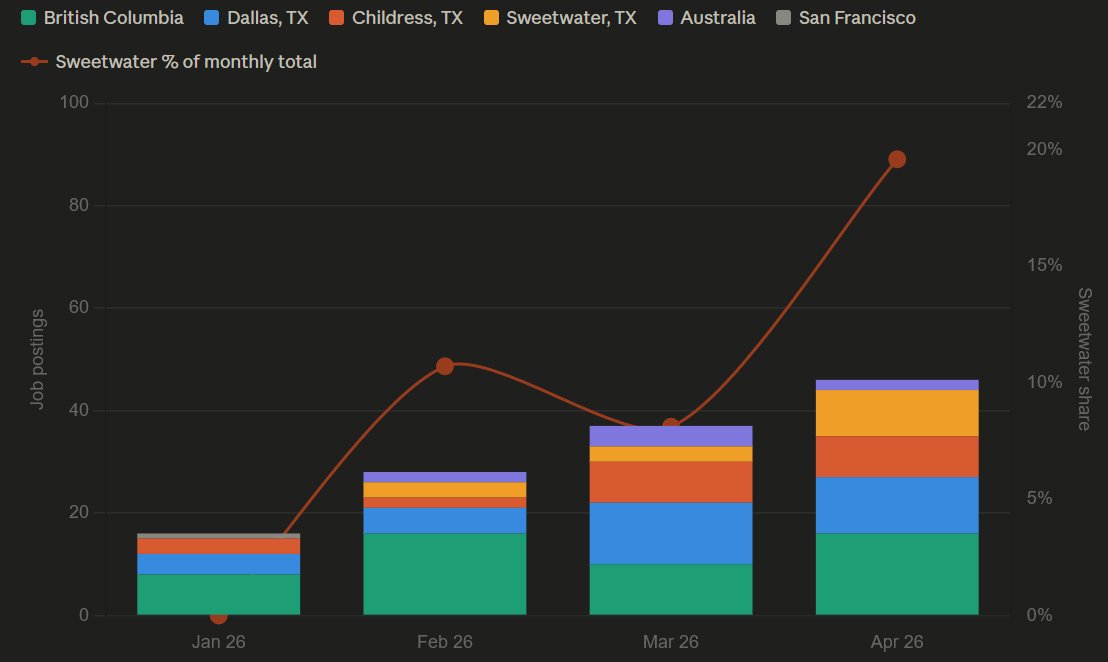

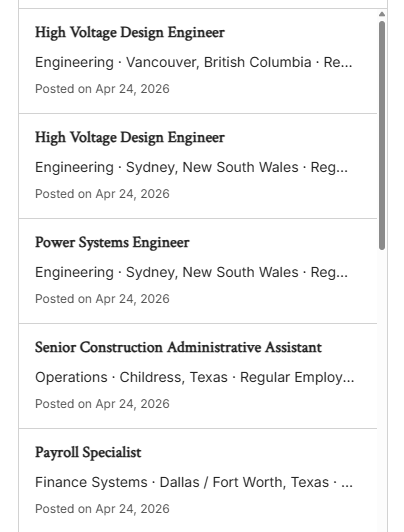

The two most verifiable signals for $IREN are (i) job postings, & (ii) construction progress. Both are real $ going out the door w/ lead time - only way to justify is w/ deals. Been disappointed to-date this year w/ % of hires going to Sweetwater - glad to see that ramping up.

English

RomainLedoux retweetledi

Where power becomes intelligence.

NVIDIA GB300s arriving at Childress for our Microsoft Horizon deployment. Big effort from the team. $IREN

Childress, TX 🇺🇸 English

RomainLedoux retweetledi

NVIDIA’s latest GPU rental prices on the Ornn Compute Price Index hit $4.95 per hour this week, up from $2.31 in early March : a 114% surge in six weeks.

The price spread over prior-generation chips doubled from $0.28 to $1.80 per hour. The new chip is NVIDIA’s B200 (Blackwell); the prior generation is the H200 (Hopper).

The B200 spot market since launch, with model release dates marked.

English

RomainLedoux retweetledi

$IREN

NEW JOB DROPS!

Look a the location of some of these. 👀👀👀👀👀👀👀

"Australian data center projects". Come on!

Tell em Dan Roberts!

English

RomainLedoux retweetledi

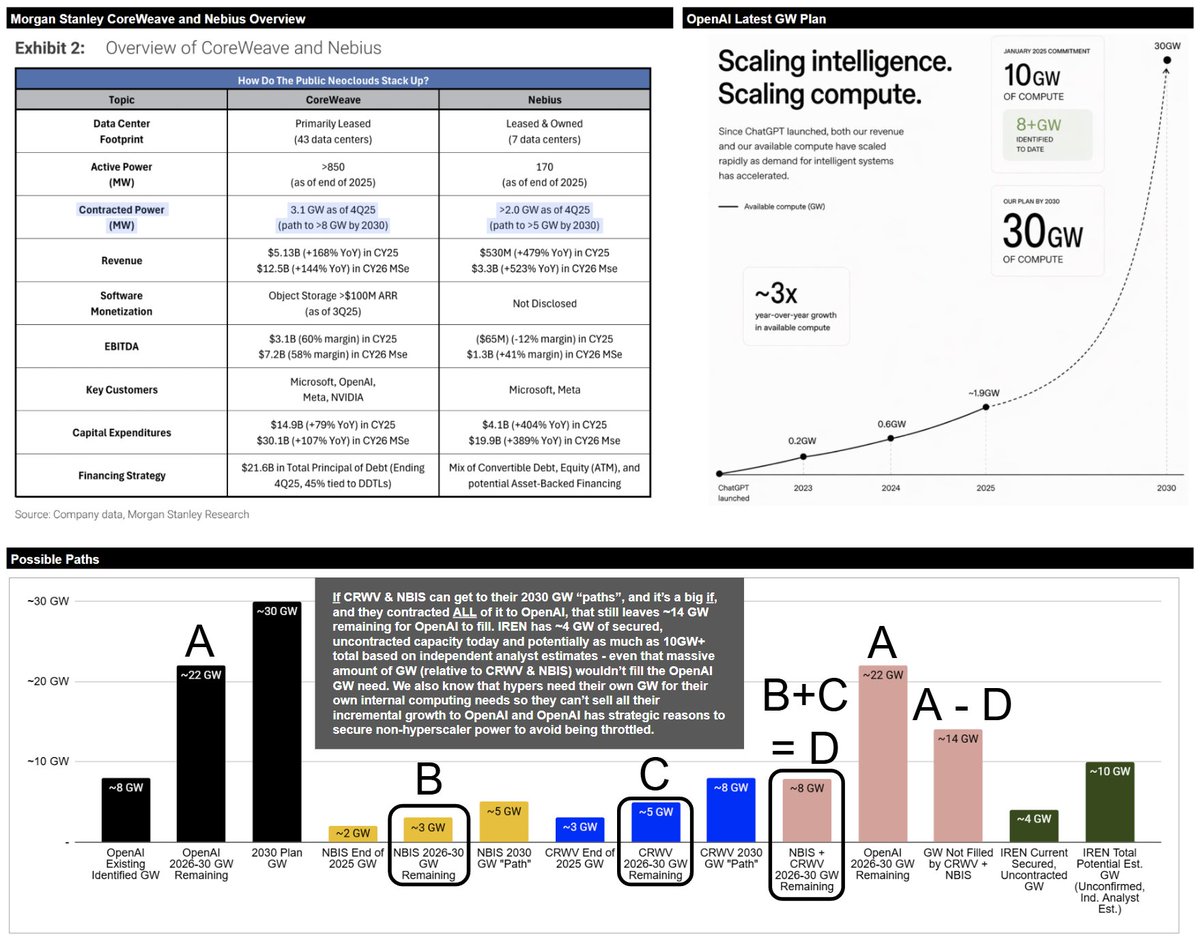

Market hasn't digested implications of new OpenAI 2030 goal. $CRWV & $NBIS won't sell all their power to OAI (& might not get there). $IREN won't sell all their power to OAI, but even $IREN's portfolio wouldn't fill it - does market still think $IREN won't contract every GW?

English

RomainLedoux retweetledi

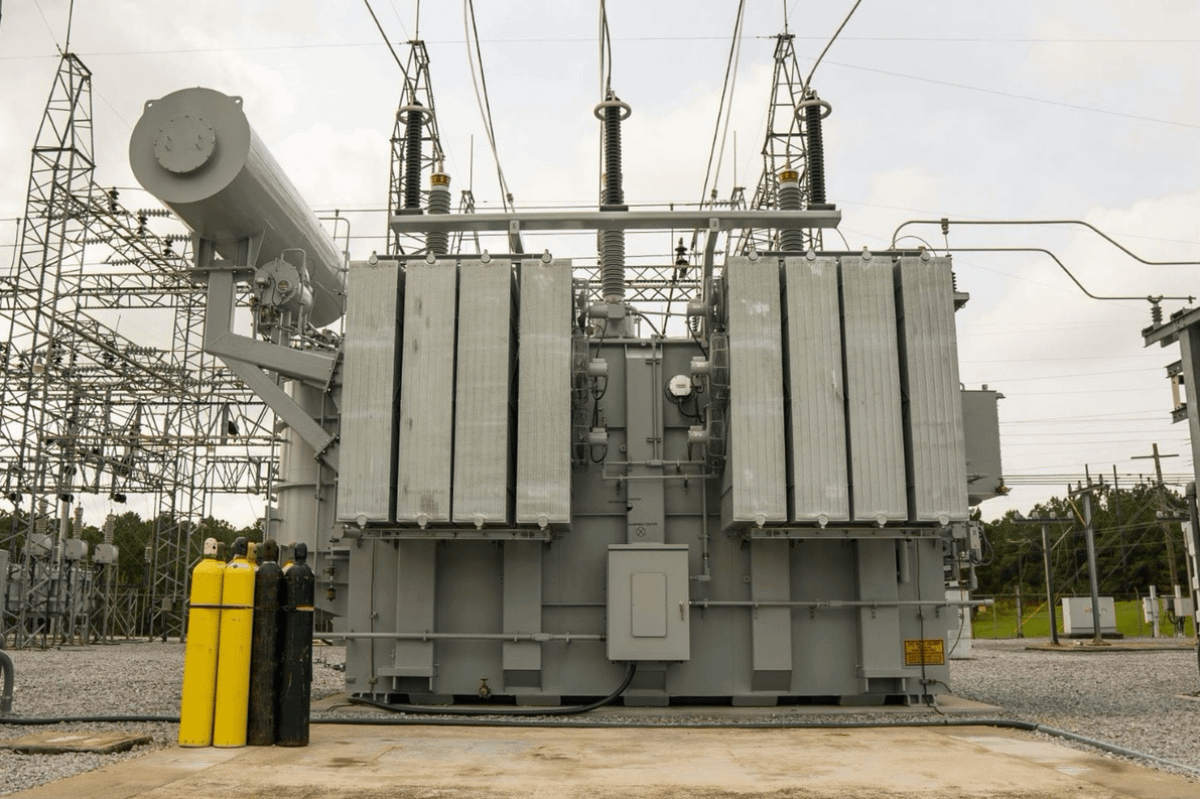

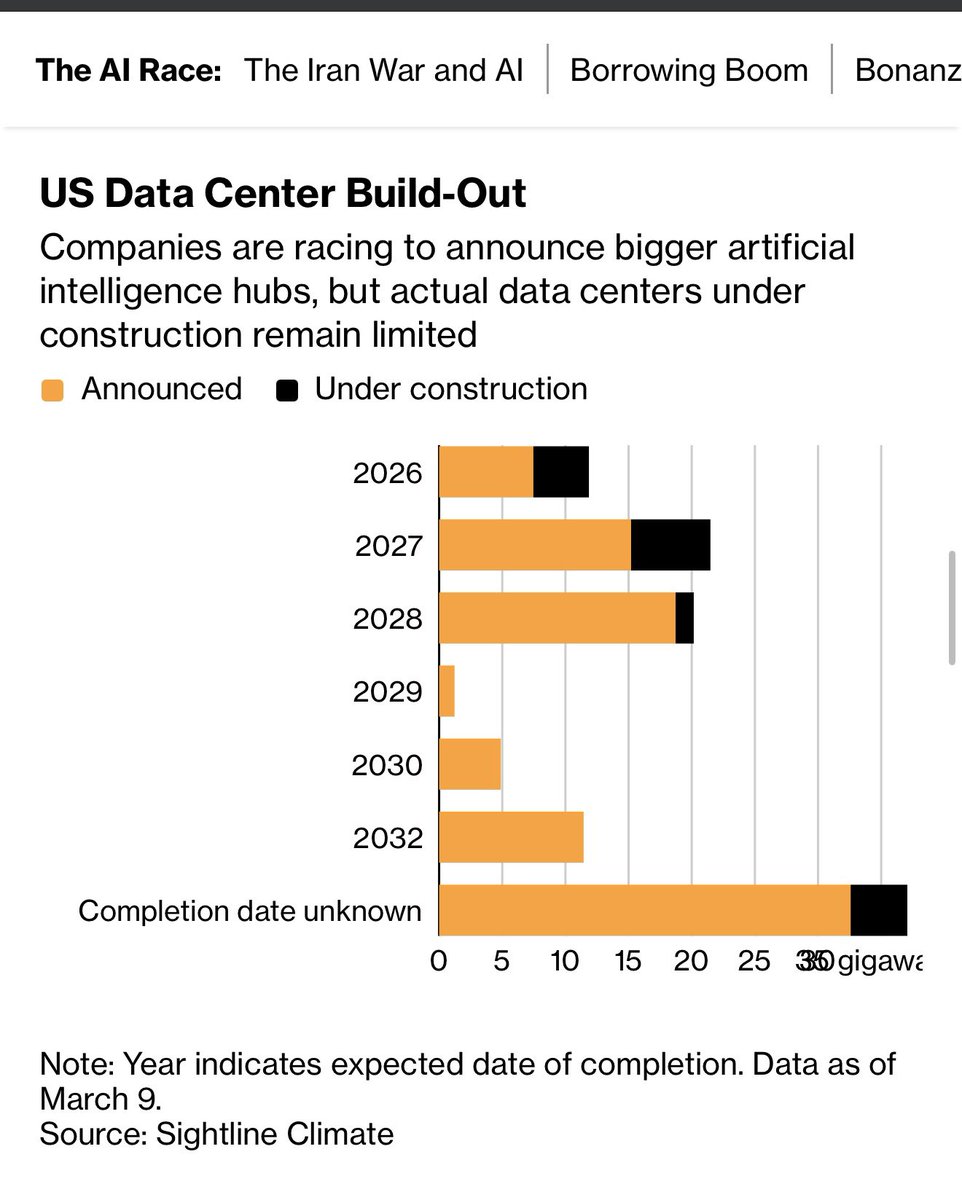

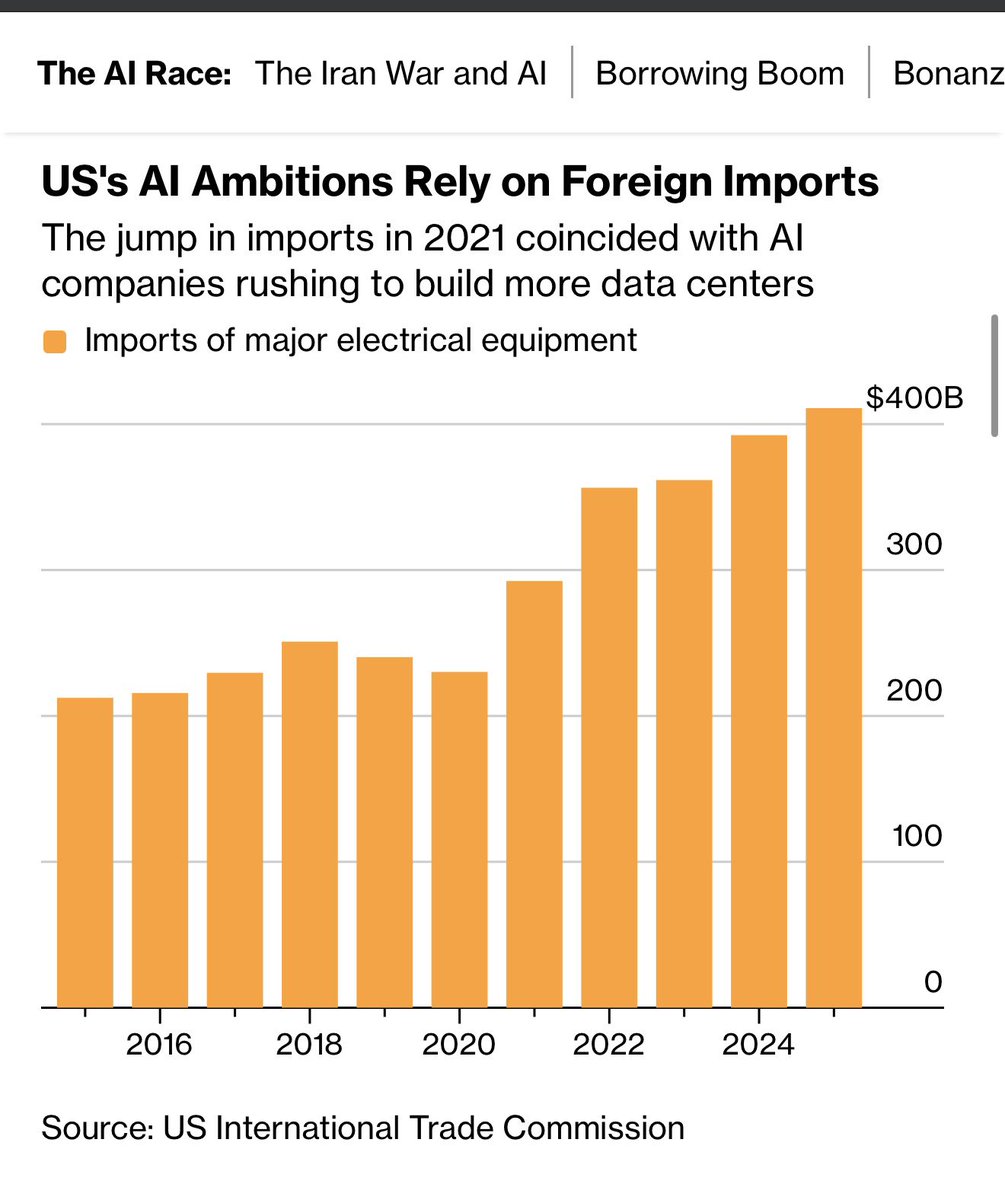

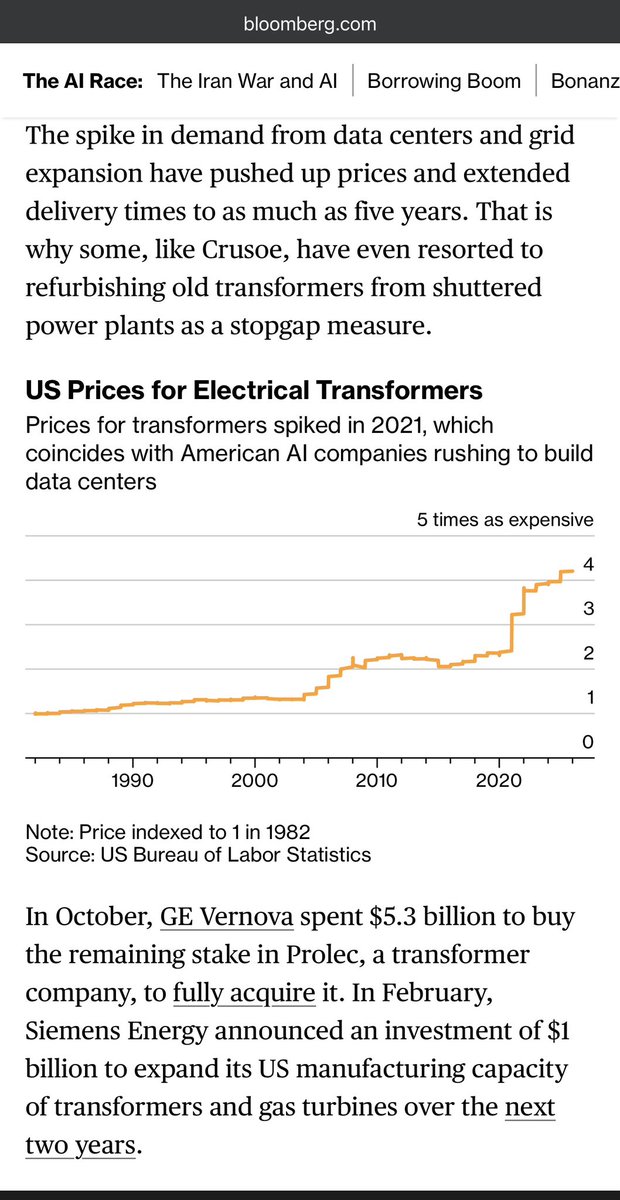

Half of America's AI data centers planned for 2026 are delayed or cancelled. They're waiting on transformers. I build chemical plants. Transformer prices have tripled in the last four years. Lead times are 2 to 4 years. Each new plant we build competes with AI data centers for the same grid equipment. Every large power transformer in America runs on grain-oriented electrical steel. It's made by rolling iron and silicon together until their crystals align in one direction. No other alloy works at utility scale and only one US company makes it: Cleveland-Cliffs. The average large power transformer on the grid is 38 years old. Service life is 40. Amazon, Google, Meta, and Microsoft committed $650 billion to AI infrastructure this year. Nvidia's most expensive GPU is useless without a transformer.

English

RomainLedoux retweetledi

It's a thoughtful, important question, and ultimately it's the #1 question investors still have as it relates to terminal value.

First let's level set on the #'s: $NBIS is targeting 3GW+ of secured power by the end of 2026 (which would put them in-line with what $CRWV has today). $IREN already has ~4.5GW secured today and that excludes the "multi-GW, international pipeline".

This is the most important datapoint that investors miss because IREN is intentionally conservative about the size of their pipeline. We know (i) they've said they could have additional sites in TX approved in batch zero, (ii) we know they're investing aggressively in ads in Australia (which they wouldn't do if they didn't have a site or sites), and (iii) we know they typically target 1GW+ whenever they can. If we assume just one additional GW in TX and one additional GW in Australia, which we could find out about as soon as this year, that would put them at ~6.5GW which is over 2x NBIS and also more than NBIS and CRWV combined (sit w/ that for a second). And I've seen credible estimates from @Agrippa_Inv @FransBakker9812 etc. that suggest the true size of the secured + pipeline portfolio could be as high as 10 GW+, which wouldn't surprise me since IREN has been aggressively pursuing secured power since before 2020. If it's truly 10 GW+, that would put IREN on par with the hyperscalers themselves in terms of the size of their GW portfolio. Sit with that for a second and remember that as we peel this question apart further below.

(As an aside, IREN trades for less than half of what NBIS and CRWV are valued at today. The GW per market cap disparity alone should be eye opening for a potential re-rate but let's stay focused on the question.)

The lead times to secure power, long lead parts, labor, etc. make building a portfolio as large as IREN's a 5+ year proposition. Absent significant M&A, NBIS will not catch IREN in the race to secure the most power & land. Which brings us to what actually happens once it is secured.

A huge difference between investors' perceptions of NBIS vs. IREN today stem purely from what each has chosen to talk about to-date. NBIS has done a phenomenal job locking up contracts and building / delivering a software solution that attracts clients. But they haven't actually built all the GW nor have they secured nearly as many as IREN (and a huge chunk of NBIS portfolio is 3rd party leased so they pay colo fees eating into their margins that IREN does not pay). IREN has been focused on securing GW of power and now building out a vertically integrated construction capability. The question that I think investors are missing about NBIS is this: can NBIS actually build out the GW they've contracted and how many more GW can they actually secure to continue scaling their business? That's a real question mark and if NBIS has execution fumbles on owned sites or third party leased sites, that is a major headwind that could dampen investor (and customer perception).

With IREN, investors are actually asking the opposite question. The question we're talking about here is: "Holy crap, IREN has a massive GW portfolio and they appear to be able to build it. What happens long term if that competitive advantage goes away because GW are no longer scarce?" Fair question, but let's be clear that it's different than NBIS questions for a reason.

Let's say hypothetically that IREN can build out the full 4.5 GW by 2030 (a stretch) and let's say they have another ~5 GW from there to build out. The existing ~4.5 GW would produce a ton of cash flow (particularly if they can re-contract powered shells that don't need to be rebuilt) and enterprise value that could be used for M&A to acquire additional capabilities. IREN already has a software solution that they're discussing w/ customers - it's just not a capability they've advertised heavily since most large scale compute customers want bare metal. But let's assume for a second they don't have that capability. M&A is always an option, and what they have today is the most scarce, in-demand resource that nobody else has at the same scale, and that gives them a lot of optionality to acquire capabilities even further up the stack (e.g., could they buy Fireworks or Together AI?). Just because NBIS has certain capabilities today (while relatively lacking the really in-demand resource which is secured GW), does not mean those capabilities can't be developed/scaled in-house or acquired over the next five years. And it's no accident that IREN just hired a senior M&A professional.

Which brings us to the ultimate question: re-leasing risk if GW are no longer as scarce post 2030 as that's the source of cash flow that gives them post 2030 optionality.

First off, the hyperscalers have been growing their own GW portfolios for their own cloud offerings for two decades now and the demand for cloud has only gone one direction. So there's nothing to suggest that cloud demand won't be there post 2030.

Second, we know that the hyperscalers themselves don't want to sign cloud contracts and prefer colo, because cloud is more expensive (which @danroberts0101 noted in the recent IREN X Space with @FransBakker9812 and @bitcoinbutcher1). That's a pretty good sign that it's the right market to be in as the cloud businesses of the hyperscalers are high margin and a huge source of their own enterprise value.

Which makes me think the obvious answer to "How do we know IREN can monetize their GW post 2030?" is this: IREN will become a hyperscaler themselves and sell cloud compute directly to enterprises (i.e., serving the same set of end customers as the hyperscalers' own cloud businesses). That is literally what @mikealfred has been saying the long term opportunity is so I have no reason to doubt it's on the potential strategic roadmap. And it's clear they're already pursuing it: why else would they be advertising so aggressively in San Francisco and Australia? There are only a handful of hyperscalers and they already know about IREN - the only logical explanation for the ad blitz is to attract the direct attention of prospective enterprise cloud customers.

Now, let's hit a few specifics around this topic.

We know from channel checks (@ShanuMathew93 posts some of the best) that enterprise cloud deployment sizes have expanded from ~10 MW to ~60 MW of late. If we assume there's not a single frontier lab or hyperscaler buying from IREN and no enterprise needs more than ~60 MW (highly doubt that), across a ~10 GW portfolio globally, that requires ~167 enterprise cloud clients. Are there that many globally by 2030 with the explosion of growth we'll likely see from AI (and other exponential growth vectors)? Probably. But the reality is, there will be much larger consumers of compute that should prefer IREN's cloud offerings over hyperscalers. Why?

Generic enterprises will at some stage be wary of the hyperscalers training their own models on customer data. Legal agreements can say one thing, but at some stage you have to ask yourself do you really want your most sensitive data on a hyperscalers' cloud if they directly benefit from using your data to train their own model? As models become more powerful, this will increasingly be in the back of enterprise customers' minds and it's an easier FUD vector for IREN to sell into over time.

The natural response to that is a shift back towards on-prem, but AI cloud compute is a much higher degree of difficulty than cloud storage, and so it makes sense to have a cloud provider who doesn't have a model themselves to fill that gap. IREN fits that gap perfectly and it perfectly positions IREN to capture cloud demand from enterprise clients who if not for the complexity of managing AI cloud compute would otherwise prefer moving back to on-prem.

But that's not all, there's another massive non-hyperscaler customer base for AI cloud compute that we shouldn't set aside: frontier labs themselves. OpenAI has built a large compute portfolio but they still need to continue scaling. And Anthropic is deeply short compute right now with their current outage issues - @DavidSacks laid this out on the latest @theallinpod episode, specifically that Anthropic has scaled ARR exponentially but is now running hard into real world linear constraints around compute (echoing what @danroberts0101 has been saying since IREN was founded).

If Anthropic and OpenAI buy compute from the hyperscalers and the hyperscalers are trying to compete with their own models, the hyperscalers can throttle the compute of the frontier labs to advantage the hyperscalers' own models, which @chamath clearly laid out. That drives Anthropic and OpenAI to either (i) build their own compute (not a core competency) and/or (ii) directly into the arms of IREN who can scale compute faster and manage it for them while not having an incentive to throttle said compute to advantage their own model.

And all of the above matters greatly to $NVDA, $AMD, etc., who all have an interest in the success of all neoclouds (including CRWV, NBIS, and IREN) to reduce their own customer concentration with the hyperscalers. And similar to the software capability discussion, it's worth nothing IREN likely has access to the same strategic financing levers with NVDA that CRWV and NBIS do which @danroberts0101 alluded to last earnings.

Finally, let's play out a 2030 scenario where demand for GW slows and IREN is competing with other neoclouds on price. First off, between now and 2030+ there's plenty of time to acquire additional capabilities to ensure that's an apples to apples fight (while others are fighting to secure GW in the next five years, IREN can take the time to develop / scale / acquire other capabilities if needed). But the more important point: IREN actually owns all its land and power so they can undercut on price because they don't need to pay colo fees. So even in the downside scenario, they have a competitive advantage to bring to bear and they can spread their opex over a larger GW portfolio which requires less of an overhead markup on their compute pricing.

(I also think as an aside that it's interesting NBIS investors tout the software capability as a differentiator when the whole goal is literally to build ASI that might make any and all software capabilities obsolete and the only thing that enterprise cloud clients might need in the future is land / power / shells / compute since the software layer itself could be ubiquitous. It's amusing to me that the question IREN faces is whether the only thing ASI can't make (e.g., land / power / shells / compute) will be less scarce, whereas competing neoclouds aren't faced with the counterfactual: what if ASI blows out the differentiation you claim in your software stack?)

If I boil all this down, the question investors are struggling with is "What happens if GW become plentiful post 2030 and IREN can't sell to hyperscalers and they have to compete on more than just bare metal?" And the answer in short is:

IREN can become a hyperscaler themselves and has spent the last 7+ years acquiring the scarcest, most in-demand resource while building the most vertically integrated capability set to scale it - they've done the hardest work up front that others haven't and now for the next 5+ years can compound that advantage. That gives them a portfolio of GW that potentially rivals the hyperscalers themselves and now over the next 5+ years it is time to become a hyperscaler by selling directly to enterprises that if not for the complexity of AI cloud compute would otherwise now prefer on-prem (vs. the hyperscalers' cloud offerings) as well as frontier labs that desperately need to avoid the hyperscaler chokehold. And while competing neoclouds (e.g., NBIS, CRWV, etc.) scramble to secure GW to compete with IREN (and likely won't be able to secure them at the same pace or scale) and avoid paying co-lo fees, IREN can take the next 5+ years to not just scale their own massive GW portfolio, but also bolt on additional capabilities above and beyond bare metal by scaling / developing their in-house offerings or simply acquiring them through M&A.

And if IREN can do that, the re-rate potential would be absolutely enormous since it would address the #1 overhang on terminal value in many investor models today.

English

RomainLedoux retweetledi

3 Imminent $IREN Catalysts

Not many companies have as much going for them right now as $IREN does.

While management has been relatively quiet since the last earnings call, I believe we're standing right before a wave of major, thesis defining announcements.

1) Australia Expansion

Given that Australia is where $IREN was incorporated, one might expect the company to already be operational there. Yet as of today, Australia remains merely the home of its HQ.

That will likely change very soon...

Just a couple of months ago, $IREN announced a sponsorship of the Sydney Swans, a prominent AFL team. As an isolated event, I wouldn't have thought much of it. The company's CEO is an Australian Football coach himself, so it could have simply been management paying homage to the company's roots.

However, this sponsorship was accompanied by a sweeping marketing campaign across Australia.

$IREN has seemingly gone all out on visual ad spend, plastering full trams with the company's logo and tagline across multiple Australian states, while also putting up new billboards outside Sydney's airport and other notables places.

Knowing how cost disciplined management is, I seriously doubt they're burning all this money on nothing. I strongly believe the company is close to unveiling a major expansion into Australia.

Currently, there are rumors that $IREN has at least two new data center sites lined up: one in South Australia, and one in New South Wales.

With how aggressive the regional ad spend has been, I'd expect any new site announcement to be accompanied by large-scale customer contracts.

If I had to speculate on who $IREN's first major customer in Australia might be, I'd wager on Anthropic, who recently announced plans to open an office in Sydney.

2) Sweetwater 1 Energization + Deal

$IREN is likely just days or weeks away from energizing its largest site to date; the massive 1.4 GW Sweetwater 1 campus.

With data center projects across the industry missing delivery timelines, largely due to an inability to secure reliable power, Sweetwater 1 stands out as a true unicorn.

Having this much grid connected power concentrated at a single site is virtually unheard of, and positions Sweetwater as one of the most valuable assets in the sector.

Successful energization will undoubtedly elevate $IREN's standing among operators industry wide, putting its execution capabilities on full display while competitors face severe delays and outright project cancellations.

Management is also aggressively hiring for the Sweetwater campus, including night shift positions, a strong signal that the company is gearing up to develop new data centers at rapid speed around the clock, 24/7.

This tells me we're likely nearing the signing of a new large-scale anchor client deal, possibly with another hyperscaler or frontier AI lab.

My expectation is that the first tranche of the Sweetwater build-out will be designed entirely for liquid-cooled Rubins, with commissioning likely sometime in H1 2027.

3) Childress Expansion

While Sweetwater is currently getting all the attention, we shouldn't overlook $IREN's first Texas campus; the 750 MW large Childress site.

So far, $IREN has contracted 40% of the site's total capacity to Microsoft, 300 MW gross across 4 tranches (Horizon 1 to 4).

That leaves 450 MW still up for grabs.

With management clearly signaling its intention to fully convert the remainder of Childress into an air-cooled AI cloud campus, the runway potential remains enormous.

Over the coming weeks, I'm expecting one of two things: either $IREN announces a new multi-hundred MW cloud contract for Childress, or management lays out a concrete plan to convert the remaining 450 MW into a large-scale cloud hub for multiple enterprise clients.

Either way, the conversion of Childress's remaining capacity is likely to begin very soon.

As with Sweetwater, the company is also actively hiring night shift HSE advisors for Childress construction, once again signaling an intent to scale development rapidly (night shift = 24/7 construction).

On a side note, I'm also expecting the successful delivery of Horizon 1 this quarter to act as a meaningful catalyst for the company's competitive standing in the market.

General Thoughts

While I've covered each of these topics in depth in previous Substack reports, I believe the time has now come for this wave of catalysts to materialize.

It's also worth pointing out that most Wall Street analysts fail to see around the corner when it comes to $IREN's cloud expansion. For the most part, they simply react to what's directly in front of them.

That means $IREN is one of the rare stocks where retail investors can front run institutional capital, getting positioned before the catalysts materialize and before Wall Street prices them in accordingly.

The irony is that over the past few weeks, retail has been doing the exact opposite: panic selling right before what I expect to be a major re-rate of the stock.

Earlier this month I also heard many investors claim that $IREN couldn't move up before new large-scale deals or other catalysts materialized…

That's a very dangerous way to think.

Markets are inherently illogical. Trying to rationalize them is a mistake not only retail investors, but institutional ones too tend to make.

Last year, $IREN's share price increased by over 1,000% from its April lows, purely on the expectation of a deal being close. If you'd waited for the actual announcement, you would have entered around $70…

In any case, with these 3 major catalysts in front of us, I'm very much looking forward to the weeks ahead and especially to the Q1 earnings call.

NFA, but I wouldn't be surprised if the stock cracks $100 in May.

Images S/O: @FransBakker9812, @tempocap2

English

RomainLedoux retweetledi

$IREN investors have been here before...

The stock cratered more than most during the recent multi-month corrective period, while lagging behind during the current recovery.

This period is eerily similar to last year's April selloff.

Sentiment was in the gutter, "wen deal" was spammed under every $IREN post, frustrated investors were calling the CEO names, and with a market cap of just ~$2b at the time, the $1b ATM that was launched in January last year seemed like an insurmountable overhang on the stock.

Contrast that with today, and we are almost at the exact same spot.

I'd even go as far as saying that emotions are more amplified today than a year ago. With the ticker having gotten more popular, there are now plenty of large accounts taking the opportunity to dunk on the stock, exacerbating negative sentiment.

As a seasoned investor, I'm unfazed by these comments. In fact, they are exactly what I'd expect during this time. If you understand market psychology, this is nothing new to you either.

Markets are predominantly driven by fear & greed.

During market peaks everyone is euphoric and throws caution out the window, while at market bottoms the inverse is true, with investors telling themselves “the market is always right" leading to them selling at the worst possible time.

Few people know that during last year's melt up from the April lows of $5 to nearly $80, I grew increasingly cautious about the overly bullish sentiment. Once we crossed $30, the ratio of bull to bear posts on X must have been at least 10:1.

Back in late August, I feared a nasty correction was imminent, one that would flush and reset broader investor sentiment.

Ironically, my cautiousness came way too early, not in time, but in price, as the stock almost tripled from that point within just weeks.

...Luckily, I don't trade in and out of my core positions, so it didn't cost me anything. But my point is that these market cycles and sentiment shifts are predictable to a great extent.

I knew we were going to get this correction.

I didn't know exactly when it would occur or at what price $IREN would peak, but I knew it was coming eventually once sentiment turned overly euphoric.

That's why this correction doesn't faze me one bit.

Now we are at the exact opposite end of the spectrum, and I believe the next leg up higher will end up being just as obvious in retrospect.

As long as the underlying asset is supported by strong fundamentals, corrective periods are nothing but sentiment resets. See it as the loading period before the next rally.

But be careful who you listen to during these times. Most investors will be emotionally shaken and unprepared, leading to irrational takes that fail to take into account important context.

Ignore the noise. Know what you own. And most importantly, don't let emotions get the best of you.

Cheers!✌️

English

RomainLedoux retweetledi

$IREN - Sweetwater 1 - Energization wen?

Iren is nearing the moment of energizing their bulk substation at the flagship Sweetwater 1 site in Fisher county Texas.

What concrete evidence do we have they are close, and what is the current state of development?

Educational post 🧵

English

RomainLedoux retweetledi

Cantor Fitzgerald just reclassified Bitcoin miners as AI Infrastructure companies. New sector, new vertical.

Their thesis: the bottleneck isn't GPUs — it's power. NVIDIA will sell ~39 GW of GPUs in 5 years. The entire US DC market used 21 GW in 2024. Almost all needs new builds.

The market is finally pricing the physical layer.

English

RomainLedoux retweetledi

$IREN: The best positioned data center company

Despite the macro turmoil of the Iran mess, compute prices are currently increasing at an incredible pace.

Nvidia's H100 GPUs, the hardware generation that came before Blackwell, are now being leased out for >30% higher prices than just a couple of quarters ago.

Keep in mind, that's an older generation (~3 years old), so you'd think prices would move down as production for the new and much more powerful Blackwell chips is ramping up.

But we are seeing the exact opposite take place. Essentially every single GPU model, both new and old, has seen an increase in leasing prices over the past weeks and months.

Demand for AI compute simply can't keep up with the available supply, particularly data center supply.

Just having access to GPUs isn't enough. Every cloud provider needs access to working data centers.

The problem is that developing modern day data centers, capable of running the latest AI hardware, comes with a bunch of bottlenecks that can't easily be overcome unless you have prepared for them years in advance.

One key factor is access to power.

Every data center needs energy to run. Yet no company can simply plug into their local electricity grid without the required permits and approvals. You first have to conduct grid studies to see if your project can be eligible to receive a constant flow of power, followed by forming interconnection agreements with utilities, and ultimately overcoming any local administrative and regulatory hurdles.

Everybody is rushing to secure power, administrative bodies are completely overwhelmed by the volume of requests, leading to greatly extended approval timelines. Therefore, securing grid connected electricity can take upwards of 5-7 years if you start today.

Plan B is to produce power yourself via on-site gas turbines.

However, this comes with a bunch of its own headwinds. It adds operational complexity, higher CapEx and OpEx, increased safety risks, as well as increased regulatory and environmental scrutiny.

Essentially you need to become an industry expert of on-site gas generation, which opens the door for the likes of $NUAI.

Once you figure out the power bottleneck, you must deal with constraints across your supply chain.

Long lead items like transformers which are necessary to convert voltage into usable power for data centers take upwards of 2 years to procure, as the rate of manufacturing can't keep up with demand. Similar to most long lead items like back-up diesel generators, switchgear, and battery and UPS systems.

Finally, there is the shortage of labor supply.

Building a gigawatt scale data center requires thousands of highly specialized workers, which are often in short supply. The AI buildout has created a simultaneous surge in demand for tradespeople across hundreds of concurrent projects nationwide, forcing developers to compete fiercely for the same limited talent pool.

All these bottlenecks are leading to issues we are seeing today: projects not getting off the ground, delayed development timelines, and outright cancellations.

Bloomberg recently reported that more than half of the data center projects planned for 2026 will be delayed. This backdrop plays exceptionally well into the hands of what I'd argue is the best positioned data center company right now: $IREN.

$IREN is one of the very few players that has been preparing for all of these bottlenecks since day one.

They started the procurement of grid-connected power 7+ years ago, during a time where virtually nobody was concerned about access to energy. As a result, the company has now secured an enormous 4.5 GW power portfolio.

This firmly places $IREN next to Google and Amazon in terms of self owned grid connected power.

Most new investors and analysts falsely label $IREN as a $BTC miner that "pivoted" towards AI cloud. But that's wrong. Since its IPO, management has consistently positioned itself as a disruptive data center platform.

…Mining Bitcoin was simply the most pragmatic way to get started and scale the data center footprint rapidly in a cost effective manner.

The founders saw the digital world would scale exponentially, with the underlying core infrastructure of the real world not able to keep up - which is exactly what's happening right now.

This is why $IREN has been securing gigawatts of power in regions of abundant energy for pennies on the dollar and with minimal friction.

This mindset and long-term strategy is why management is constantly ahead of the curve when it comes to securing long lead items years in advance for sites that have yet to energize.

I remember back in 2024, when management talked about having secured long lead items for its Sweetwater campus whose energization date was 2 years away. Today $IREN is reaping the benefits of that calculated decision by being on track to energize the 1.4 GW project this quarter, positioning the company with one of the largest grid connected data centers in the world.

In essence, $IREN is much more than just a regular cloud provider. It’s effectively the only fully vertically integrated cloud platform that exclusively houses its GPUs in self developed data centers.

The real advantage here isn't just improved cost structures, but that management has a much greater degree of control over its own destiny.

As the head contractor of all of its data center projects, $IREN controls everything from supply chain management to sourcing labor. If one aspect of a buildout is facing unexpected delays, management can quickly allocate labor and resources towards another section, significantly reducing the risk of delays.

There are simply no other cloud providers with this level of control and flexibility over their pipeline development. And in a world that is severely compute constrained, these attributes are worth gold.

Demand is accelerating, supply can't keep up, and leasing prices for GPUs are skyrocketing. $IREN is in a very unique position to capitalize on these market circumstances in a major way.

The market clearly hasn't fully priced this in yet.

English

RomainLedoux retweetledi

Our run-rate revenue has surpassed $30 billion, up from $9 billion at the end of 2025, as demand for Claude continues to accelerate. This partnership gives us the compute to keep pace.

Read more: anthropic.com/news/google-br…

English

English

RomainLedoux retweetledi

fantastic story. fantastic charts.

Akshat Rathi@AkshatRathi

Half of US data centers planned for 2026 are expected to be delayed or canceled. One big reason is shortage of electrical equipment, such as transformers, switchgear and batteries. US doesn't have manufacturing capacity, forcing it to rely on imports. 🎁🔗 bloomberg.com/news/features/…

English

RomainLedoux retweetledi

At GTC this week we spoke to everyone in the neocloud industry. Hopper contracts coming due are being renewed for multi-year terms at significant price increases. Most of the Blackwell capacity coming online this summer is already spoken for.

Customers are fighting to pay $14/hr for p6-b200 spot instances in AWS and you're bearish??

English