TheDancingMonkey

464 posts

TheDancingMonkey retweetledi

If $LMND literally stopped acquiring customers today and let the book run off to zero, here is what you own:

Q1 2026:

1.33B IFP

85% ADR

62% GLR (39% gross margin on GEP)

1.14B cash and investments

Total premium pool: 1.33B / 0.15 = 8.9B

Gross profit at 39% margin: 3.5B

Runoff OpEx: 0.5B

Net underwriting value: 3.0B

PV at 10% discount: 2.1B

1.14B cash and investments

0.25B IP and licensing value

Total runoff value: 3.5B

76.8M shares outstanding puts the floor at 45 per share.

At 51 today you are paying 6 per share for one of the fastest growing AI companies on the planet with 10 consecutive quarters of accelerating IFP growth, FCF positive for the first time, Car growing 60% YoY, Pet crossing 500M IFP, autonomous Car product converting at 70% higher rates, and an insurance OS that Shai Wininger just called paradise for AI agents.

The runoff value is the floor.

Everything above it is optionality on AI eating a 500B industry.

That optionality is currently priced at 6 per share.

The margin of safety is staring our in the face. 🍋

English

What’s a stock that’s STILL down big that you’re picking up right now?

English

What is one stock that can double in the next year?

English

$RKLB is the safe play in my portfolio, not the risky asset.

That’s what the other 20-25% is for.

Chris Ray@itschrisray

Pretty happy with my portfolio mix right now, even if it is a little heavy on the $RKLB. 😅 $RKLB $ONDS $OUST $LMND $P $KOPN

English

TheDancingMonkey retweetledi

Did $LMND just roll out it’s third state for renters in ~ a week? Yes they did.

They accelerate growth even without state expansion and this is definitely pushing the numbers further.

Glad to be a long term investor, we are just in the beginning.

English

TheDancingMonkey retweetledi

@Neil_X10 @Leinad7331 This is from one of the larger Scandinavian brokers. Number of shareholders this year.

English

@Leinad7331 Do you have a view of the retail ownership?

My sense is that it spiked in Jan (TSLA partnership announcement) and has been on a steady downtrend since.

English

Institutions are accumulating $LMND in the $50-$60 range.

Neil 𝕏@Neil_X10

Stocks like $LMND with high retail interest look like this across the board (share price down / institutional ownership up) It isn't a coincidence.

English

I started a new position today.

This will be one of the largest position in my portfolio once I finish building it out.

High conviction - only.

English

TheDancingMonkey retweetledi

I think the team delivered a stellar set of results!

I think the market is rotating into semi-conductors and there is fears around information based economies (which I personally believe is overblown for insurance personally) - insurance holds regulatory and capital moats and if any company was going to be at the forefront of the displacement - it’ll be LMND.

I think the timing of the SBC was highly unfortunate, and it dilutes a lot more than I would personally like, epically over the next couple years - the flip side of this, is that the structure of it being in options - will generate 10’s of millions of cash for them, supporting growth and capital adequacy.

Leadership setting up a preplanned agreements is nothing new - and most of the time they hardly use them if at all, and it’s sensible for them to have it in place in case, but it’s never nice to see…

If they were wanting to raise cash via the use of options - they should offer it out to retail or similar mechanism. They would likely get a shit load more cash and would help make sure that the people over here that have supported and believed in them since day one don’t get diluted so badly 🤷♂️ - it’s painful to watch the whole market run and see LMND lag - but it’s still up 203% over the past two years… I’ve always said I’m in this for the long term 10+ years unless something material changes… it’s not as far as I’m concerned.

Even accounting for the SBC, their growth and fair value per share today still sits somewhere between $170-220 depending on what assumptions you make…

I’ve spend many evenings the past few weeks reviewing Serffs to do a comparison between Root and I’m still fair more bullish on LMND long term

English

TheDancingMonkey retweetledi

On the matter of SBC for Daniel and Shai:

This is not a normal option grant.

Each received 180,000 RSUs, so 360,000 potential shares in total. But these shares only vest if $LMND closes at $110 or above for 30 consecutive trading days within 24 months from the grant date.

If that stock-price condition is not met, the RSUs are forfeited.

So economically, this is a very performance-heavy equity award:

No $110 stock price → no shares issued from these specific RSUs

$110 for 30 straight trading days → shares vest → dilution happens

That part is actually shareholder-friendly in the sense that dilution only occurs if the stock has already performed very strongly.

But the accounting treatment is the part many investors may overlook.

Lemonade assigned these RSUs a total grant-date fair value of $15.4 million using a Monte Carlo valuation. The company then recognizes the stock-based compensation expense over the derived service period, regardless of whether the $110 stock-price hurdle is ultimately achieved.

In other words:

For dilution, the award is conditional.

For the income statement, the SBC expense still runs through.

If the stock never reaches the $110 hurdle (in the 24 months), the RSUs can expire worthless from an ownership/dilution perspective — but the SBC expense that was already recognized is not reversed.

That creates an important distinction between economic dilution and accounting expense.

The market-condition RSUs are therefore not necessarily “bad” by themselves. They align management with a much higher share price. But they do add non-cash SBC pressure even before shareholders know whether the performance target will ever be met.

For $LMND, this matters because stock-based compensation is already a meaningful item. Q1’26 SBC was $21.2 million, up from $10.3 million in Q1’25. The new market-condition RSUs contributed only $0.6 million in Q1, but total unrecognized SBC related to these market RSUs was still $14.8 million at quarter-end.

English

@Ironic_Ape @OGCapital25 @ASchulz888 Would love your honest take on the earnings and the current situation.

English

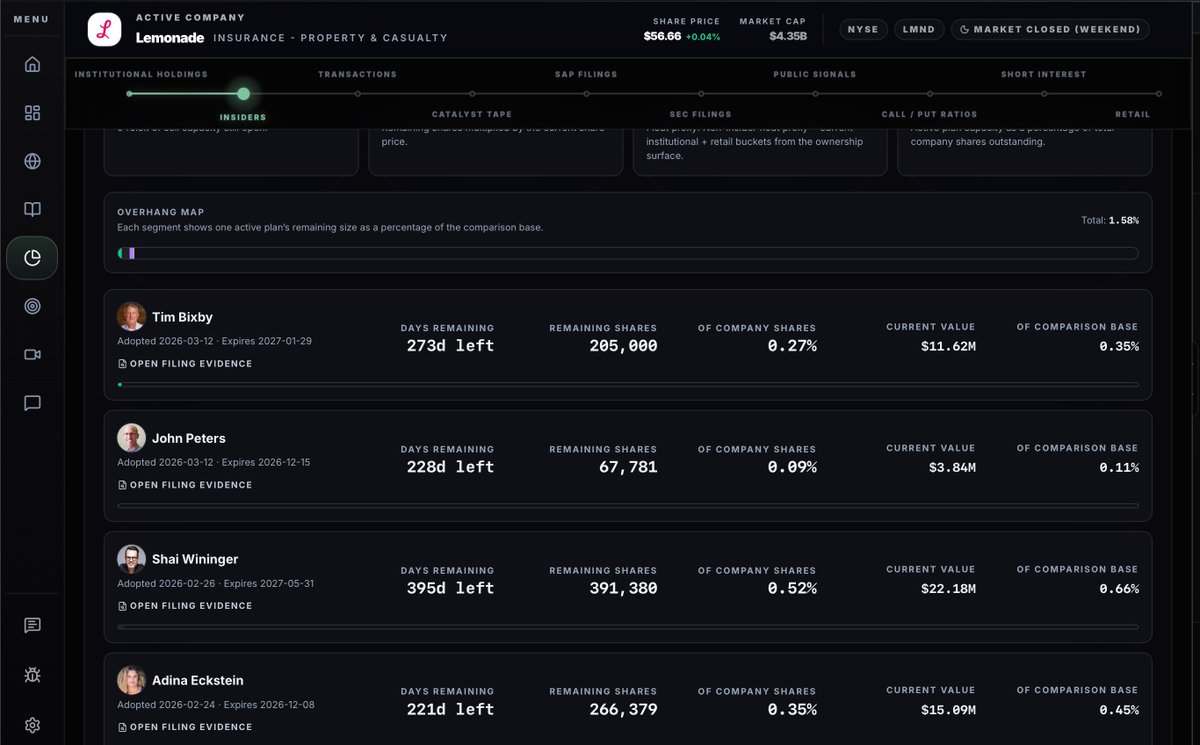

@OGCapital25 @ASchulz888 They did file for them a while back - all combined a little less than 1.6% of the company.

They also get a lot of their SBC as options, so if you look at Adina for example - she typically sells stock to buy options…

English

Dear management teams,

If you want to max your SBC, remember you need your stocks up.

If

(1) Your stock is in a large drawdown

(2) You granted yourself a large new SBC in 1Q26

(3) Days later all senior leaders file 10b5s to sell stock.

How exactly should shareholders feel?

English

@Erifra2 Rough seeing so many pre revenue stocks rip while $LMND tanks.

English