Read this article carefully and then examine $LMND’s LTV/CAC unit economics and then invest accordingly … it could make you a fortune.

**not financial advice**

Pranav Singhvi@pranavsinghvi

English

Paper Bag Investor

10.3K posts

@PaperBaglnvest

I search for high-conviction, multiBAGger investment opportunities. Explore every angles,deep research , then invest big. 29% CAGR since 2009. IT'S IN THE BAG

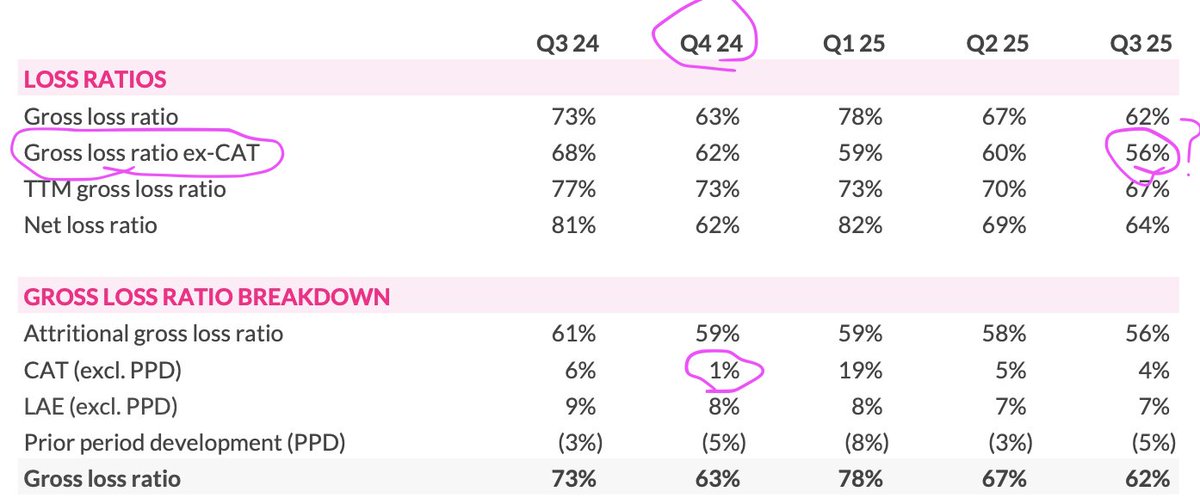

Loss Adjustment Expense (LAE) may go to 3% range as they scale larger. As per graph from Q3 letter.

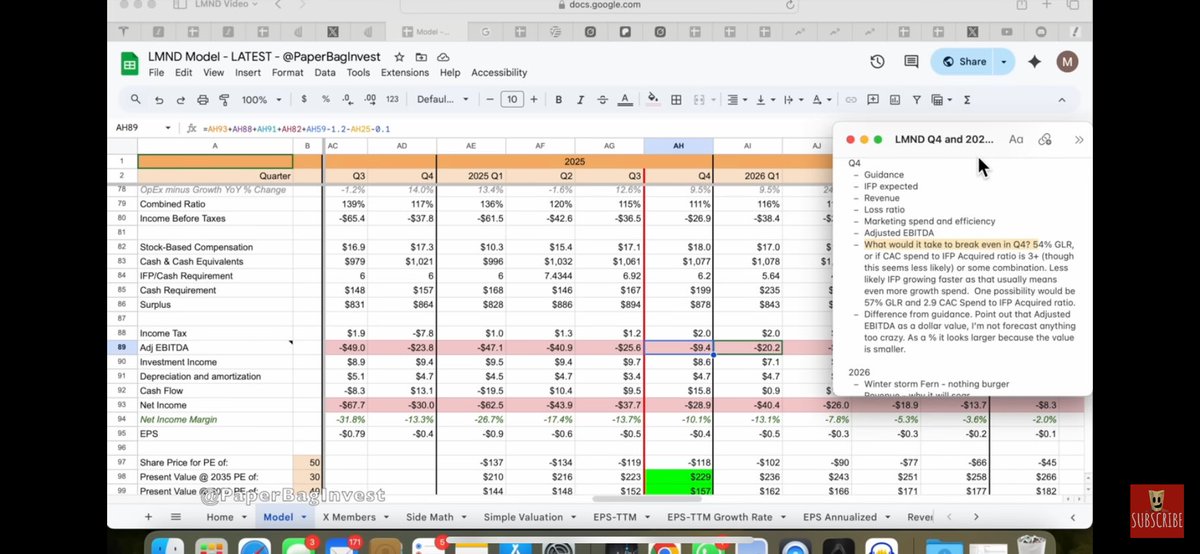

I know many are trying to explain the (so far) big drop today. It is pointless in my view. Algos, manipulation, tourists, or all of the above. Who knows? And it does not make any difference whatsoever. The results were amazing. The potential energy keeps accumulating. The eventual rise will be great for investors. And there is one big issue I don't see anybody talking about today: a big, BEAUTIFUL CHERRY on top of Lemonade's guidance for 2026. Or at least that's what I see. I have tried to adjust my model to reach -48 million in Adj. EBITDA for 2026 (as guided). Can't do it. Unless we get horrific CAT events in Q2/Q3 (LA-fires-kind of events). I think that is very unlikely. With a cleaner book and better AI-LTV models, very unlikely. The best (or should I say worst) I can do is -20 for the year. But I can also see a realistic path for -1. We are so close to zero and revenue is growing so much that small changes have a big impact in the bottom line. Take into account that we are just at -2% Adj. EBITDA margin! With -20 Adj. EBITDA in Q1 (guidance is -22) and positive Q4 (I have it at +11, in a worst case), that leaves Q2 and Q3 for the difference. Simple math -20+11=-9 That would mean -39 million for Q2 and Q3. In other words: Q1 (which is usually the worst month) equal to Q2 and Q3. Even if we have worse GLRs in Q2 and Q3 than in Q1 (forecast), just with the operating leverage of the much higher revenue in each quarter and flattish Opex, we would get a much better Adj. EBITDA than in Q1. (Yes, I am taking into account the increase in growth spend.) So I am calling it. Unless we get a monster, LA-fires-like CAT event this year, Adj. EBITDA for the year will fall between -1 and -20 million. A huge beat over guidance. Also, with enough luck, if we get a stellar Q4 in 2026 like we just did for 2025, we might even be on the brink to the first EPS breakeven in Lemonade's history. It's a stretch, but not impossible. Let's have a great 2026, regardless of Mr. Market's tantrums.

Enough is enough. Got the green light from the Mrs and dumped half the $TSLA position just now, bought a significant share count of $LMND. Q4 earnings are in a week and 2026 will be a pivotal year in my opinion. Life is too short to be a chicken.

Video is public! The Ultimate $LMND Q4 and 2026 Preview 🍋 youtu.be/TsJriFRqZ6k

Video is public! The Ultimate $LMND Q4 and 2026 Preview 🍋 youtu.be/TsJriFRqZ6k

@PaperBagInvest , I’m honored to be featured in your video at the 53 minute mark 🙇 A few thoughts on the 2026 IFP guide that I don’t think you brought up: - I think the 2026 IFP guide will be at least 30 percent, as management has stated before. - Over the course of the year, I expect we’ll see beats where IFP reaches 32-33% growth in certain quarters, especially as FSD car insurance expands to more states. - The FSD insurance product is so differentiated that I think CAC spend will be very low for most customers. We already see that momentum in Google Trends, and legacy players won’t catch up anytime soon. - Even if the stock doesn’t move after the Q4 report on Feb. 19, I strongly believe 2026 will be a great year and that $LMND will at least consolidate in the $120 to $130 range. Thanks again for everything you do. You’re the OG $LMND retail investor.

Just dropped my old insurer—$350/month. Dropped without notice over a clerical error. Leveraged @Lemonade_Inc this morning for my ’22 Tesla Model 3 in CO. Bug hit during app quote, called in and rep crushed it, devs fixed in under five hours. Now insured for $122/month! Killer UX, better coverage, and hyped for @Tesla direct integration. Switching to LMND! 🚀🔥 #LemonadeInsurance @shai_wininger @farzyness $lmnd @PaperBagInvest